The following resource is designed to help teachers, reporters, policymakers, or anyone interested in learning more about teacher pensions. If you have additional questions that are not answered here, please contact us teacherpensions@bellwethereducation.org. We will continually update this page to help our readers.

- What is the average teacher pension? Here is our state-by-state chart, or more detailed looks at the average teacher pension in Illinois and California. Keep in mind that simple averages often don’t tell the whole picture.

- How generous is my state’s pension plan compared with others? To see how your state compares, see how much your state is spending on teacher retirement benefits.

- Where can I learn more about a particular state or municipalities’ pension plan? How much do teachers contribute, what’s their cost-of-living adjustments (COLA), when do teachers need to retire? To find more information about pension plan components, check out your state's teacher pension plan website, browse through the TeacherPensions.org state pages, or scan the Urban Institute's State of Retirement Report Card.

- How much do teacher pension plans cost? Check out the Public Fund Survey to examine funding levels, assets, liabilities, and other related information for the nation’s largest pension systems from 2001 to present. To see how much teacher pension plans costs by state, see here or see our report on the "Pension Pac-Man" for how pension spending translates for the average teacher.

- Where can I learn more about pension reform options and possible solutions? Read this handbook from the Reason Foundation to get a primer on possible options. Pension reform need not be limited to just a 401k-style plan and there are number of other alternatives for policymakers to consider.

- Where do I find more information on teacher retention in each state? State and municipal pension plans hold a wealth of data on their members, including calculations and projectios on teacher retention rates. This report from TeacherPensions.org and Bellwether Education Partners uses actuarial assumptions to estimate teacher turnover rates in every state. See this compiled chart from NCES' Schools and Staffing Survey for data on teacher experience levels in your state. For nationwide trends in teacher retention and turnover, see this post, or this post on how the teaching workforce is simultaneously older but less experienced.

- Which teachers receive Social Security, and why do some states not participate? For more information on teachers and Social Security, see this TeacherPensions.org report. Over 1 million teachers do not participate in Social Security and are concentrated in 15 states: Alaska, California, Colorado, Connecticut, Georgia, Illinois, Kentucky, Louisiana, Maine, Massachusetts, Missouri, Nevada, Ohio, Rhode Island, and Texas and the District of Columbia. See here for a quick history and explanation for why teachers don’t participate.

Last updated on 3/9/2020.

Taxonomy:As a country, we spend hundreds of billions of dollars a year on tax incentives for individuals to save for retirement--including employers that contribute toward those accounts. But do those incentives actually work? Do they change people’s behaviors? Are people satisfied with the results?

A new paper from William G. Gale, Benjamin H. Harris, and Claire Haldeman surveys the landscape and finds that we don’t have good answers to these questions. They write, “policymakers do not have access to robust empirical consensus when making decisions that affect the retirement security of tens of millions of families.”

I spoke with Harris about these findings and his ideas for a research agenda to begin to answer questions about how Americans experience retirement. What follows is a lightly edited transcript of our conversation:

Aldeman: Can you give us a brief background of the paper. What were your goals in writing it?

Harris: I think that Americans hear a lot about retirement saving, and there’s a lot of anxiety about people being poorly prepared for retirement. Part of this has to do with some of the information that’s coming out of the financial services sector, part of it is the information coming from policymakers, part of it has to do with concerns about Social Security solvency, and part of it has to do with rising health care costs. For whatever reason, there’s a lot of anxiety and misinformation about Americans’ preparation for retirement.

The point of this paper was to lay out a case for ways we can learn more about retirement and try to provide a pathway for policymakers to know more about ways to improve the retirement experience. We’ll get into the details later, but our idea was to say, “there’s a lot we don’t know about retirement, here’s how we can get to place where we know more.”

On that front, you write, “almost no retirement policymaking is rooted in evidence; programs simply continue indefinitely with little or no Congressional oversight.” That’s a striking statement. Can you say more about what you mean by that, and what the implications are?

Sure. The predominant form of subsidizing retirement saving in this country is through 401k-type plans, also known as defined contribution plans. These are plans where people get a tax exemption when they put the money in during their working years, the money grows tax-free, and then is taxed when people take out the money in retirement. There has been very little attention by policymakers to whether or not these types of plans are actually working. By “working,” I mean whether or not they’re boosting households’ savings.

Now, we know there’s money in these plans, trillions of dollars. But the key question is whether or not they’re actually inducing Americans to save more. Someone could ask, “why does this even matter?” Well, it matters because we’re foregoing hundreds of billions in tax revenue every year in order to subsidize this type of saving. So the first big question is whether these plans are working, if they’re leading to higher rates of saving by Americans.

The second general question is about how Americans spend down their retirement savings. Even thought someone might accumulate a lot of money in these plans, we don’t know if it leads to a better retirement. Does it allow them to retire when they want to retire? Does it allow them to take care of the heath costs that they need to take care of? Does it allow them to not be a burden on their children, if that’s what they want?

The basic point is we’re giving hundreds of billions of dollars in tax breaks every year. Maybe we should pause to ask, “are these really working?”

When we’re talking about retirement savings policies in this country, other than Social Security, we’re mainly talking about tax policies. But is the tax code the right lever to encourage retirement savings?

That’s a great question. With retirement, we often talk about a three-legged stool, which refers to Social Security, private savings, and employer-provided retirement accounts. The tax code is the major lever for all of these. Workers get big tax breaks for saving in their pensions or 401k-type plans. Returns on saving outside of retirement accounts are taxed at lower rates, and the tax rate is zero on gains held until death. Even when we’re talking about Social Security, there’s a tax element as well, because retirees are taxed differently on their Social Security benefits than they are on other types of income.

The tax code is the lever for much of our retirement policy. I think it’s a good question to ask whether we should think this through better, and evaluate whether it’s working as well as it could. It doesn’t have to be this way. Medicare is an example of a different way. Medicare does not have a big tax aspect to it, and it seems to be working well. So this tax issue is an open question and one we think worth considering.

Could you talk a bit about the power of defaults? There’s a lot of work showing that “nudging” people into better retirement savings habits materially changes their behavior. Should we just create more nudges, or how should we think about nudging in this context?

This is the big innovation in retirement saving, or in saving more broadly, over the past 10 or 15 years. Thirty years ago we thought it all came down to incentives. If we gave people a plus-up, some financial benefit for saving, that was really all we needed.

There are a couple problems with that. The first is that the structure for savings are “upside-down.” By that I mean that if you’re in a higher tax bracket, your incentive for saving is higher. Each dollar you put into a retirement account is subsidized more than someone in a lower tax bracket. And if you’re not paying much in income taxes, there’s also an open question of whether you should be explicitly saving for retirement at all.

The research on nudges has helped us realize that incentives can be unequal, and that incentives sometimes just don’t work. There’s a study we reference in the paper by Raj Chetty and his co-authors where they looked at Denmark {Note: see the paper here}. The reason that Denmark was a good country to study is that they collect data on every retirement saver in the country. They also had big changes to their retirement policy that made it possible to study people’s behavior. One of the interesting findings that came from the study was that it classified people as either being active savers or passive savers. They defined an active saver as someone who was paying attention to incentives and then responding to them. They found roughly 15 percent of people to be active savers. But if only 15 percent are really paying attention—and this is Denmark, so it could be different than the United States—then incentives don’t matter that much, because people don’t know about them and can’t respond to them even if they wanted to.

Automatic saving is a way to get around that. The idea is that if you automatically put people on a sound savings path, people largely stick to that. There are some problems with that, of course, which we can talk about. But in general there’s been a shift in the thinking around retirement due to this type of research. If it’s the case that incentives don’t work that well, then automatically nudging people onto the right path is a more effective strategy.

You mention the Chetty study on Denmark, and it’s clear in reading your paper that much of what we know about retirement savings come from European countries. Can you comment about why that is, and whether the studies on Europe are applicable to the United States?

A lot of time we need a change in policy to study whether a policy works. In Denmark, it was helpful because we could see how people responded to a change in incentives. In the United States, we don’t have those same natural experiments to study the impact of savings incentives.

The data here in the U.S. is another problem, and it’s becoming worse. People are getting saturated with surveys, they’re distrustful of people asking them about their personal information. I think that’s a perfectly reasonable response to developments in privacy, but the drawback is that the public surveys that we rely on are deteriorating in quality over time. It can be very difficult to find a quality dataset to study retirement security. If we had data like Denmark’s, then we would know much more about the effectiveness of incentives here. We don’t even have to go as far as Denmark, where they collected data on every single person in the country. Even if we just had a high-quality sample of people showing how their saving evolves over their life path, that would be tremendously effective in our understanding of retirement.

In the paper you lay out a couple different paths for developing a research framework to evaluate our retirement policies. What sort of systems would that entail? Or how would we get to the vision you’re putting forward?

There are three things we lay out in the paper, and they all seem pretty achievable. They’re not all that expensive, in the millions and not the billions, which is relatively small on the federal level.

The first step is that we should evaluate tax expenditures. In the context of retirement savings, tax expenditures are mainly the tax breaks we give for putting money in a 401k or, for an employer, offering employees a pension. These have never been formally evaluated, which may be surprising given that we’re spending over $200 billion a year on them. Maybe we should pause for a second and evaluate whether they’re actually working. Private companies regularly take a step back and ask whether their strategy is working, whether that’s in retail or tech or finance. We think the government should do the same thing. There are a couple agencies within the federal government that are well-suited to evaluate tax expenditures. What we should have is a formal, ongoing process whereby government evaluators periodically study whether our policies are working.

The second thing we call for is a 1 percent carve-out for program evaluation. This has long been a priority of Results for America, where I am affiliated and which was a sponsor on our paper. The idea is, for programmatic funding, we should carve out 1 percent for evaluation. That could be everything from randomized control trials (RCTs), where you assign a treatment and control groups and evaluate whether a given intervention had an effect on the treatment group. But it doesn’t have to be RCTs. The fundamental idea is to set aside $1 for every $100 in spending towards formal evaluation of programs to see whether or not they’re working.

We specifically called out the Social Security Administration. To be clear, we’re not talking about 1 percent of all the dollars spent on Social Security. We’re talking about 1 percent of all the dollars spent on administering the program, which comes down to $1 out of every $7,000 spent on the program overall, including both the disability and the old-age program. Devoting that 1 percent toward program evaluation might help us understand more about how the program is impacting retirement.

The last thing we thought would be a good idea would be to put together a dataset that approaches what Denmark has. It would be a panel dataset that would follow households over time. It would link administrative data that the government already has on people’s participation in different government programs, as well as tax data and survey data that people report. The survey questions might include answers to questions like, “when do you want to retire?” “how do you feel about your retirement?” or “how healthy are you?” Having a dataset combining all those elements would allow us to know so much more about retirement, and that would allow policymakers to make reforms that ultimately make people better off in the long run.

It doesn’t take a lot of money to do this. If we siphon off just a little bit, 1 percent from each program, we can make the programs much better.

What are the biggest barriers to implementing this vision? Is it cost, inertia, fear of privacy, or what are the biggest obstacles?

This is a great question. If I had to rank the problems, I would say the biggest one is what do you do when you find out the program isn’t working? What do we do if we find out that 401ks aren’t as successful as we thought? It’s tough to make policy decisions in the face of finding out that a program is ineffective. People like most programs, even if they may not be working all that well. That’s a big challenge.

A second challenge comes down to funding. Even though 1 percent seems like a small number, we are budget constrained these days, and policymakers are always looking for cuts. Even a 1 percent add-on could feel like a tall order.

The last thing I’ll say is on the data. We’re fighting this sea change on survey data. If you look at some of the work by Bruce Meyer and others, who have found that the rates of response are plummeting over time {Note: see the paper here}. It used to be that we’d see response rates of 60 or 70 percent. Those have been cut in half, and there are some questions some people are just no longer comfortable answering. People are reluctant to answer questions about their personal finances, and people don’t love that the government has this information and they’re sharing it with researchers.

Everyone understands the importance of paying taxes, but there’s sometimes an expectation that that information stays with the IRS. When the IRS does share information, it’s incredibly powerful from a research perspective. Some of the best papers we’ve seen over the past 10 years, including papers written by Raj Chetty’s team, have come out because they had access to IRS data. But the IRS is so careful and cautious with the data it can be a barrier to implementing our third pillar.

Are there any other points you haven’t mentioned?

The last thing I’ll say is that in addition to a shift in our understanding of incentives versus nudges, there’s also been a big shift between the saving process and how we spend down assets in retirement. We’ve shifted from a world in which everyone got a pension, or at least most people who got a retirement benefit through the workplace had a pension, to one where we’re mostly just saving on our own in our individual accounts. The implied expectation seems to be if you saved enough you’d be okay. With expanding longevity and high out-of-pocket health care costs and other sources of uncertainty in retirement, we need to focus not just on how much you have saved in your 401k, but also on strategies for spending down those assets. Economists call this the “decumulation” process.

That means retirement is not just about understanding how people save, but also the strategies people use to spend their nest eggs that they spent their whole life accumulating. Do strategies like reverse mortgages make sense? Should people buy annuities? Should we think about a better market for long-term care insurance? Those types of questions are only going to get more and more important as Baby Boomers get deeper and deeper into retirement.

Taxonomy:Teacher pension systems are not structured to effectively serve educators whose spouse is an active duty military service member. And while teaching may be a good career option for military spouses in theory, the way that states have set up their pension plans means these families will face challenges saving for retirement.

For military families, who typically move every 2-3 years, the problem can be boiled down to this: statewide defined benefit (DB) pension funds are designed for educators who spend their entire career teaching in the same state. A key challenge for highly mobile educators like military spouses is that state teacher pension benefits are not portable. Teachers who leave the state, even if they continue teaching elsewhere, cannot take their pensions with them. This is not to say that teachers who have served long enough to qualify for a pension lose those benefits if they move away from the state. Rather, their overall pension wealth ceases to grow once they leave the state. Dividing a career’s worth of pensions across multiple state plans can significantly decrease the total value of their aggregate retirement wealth.

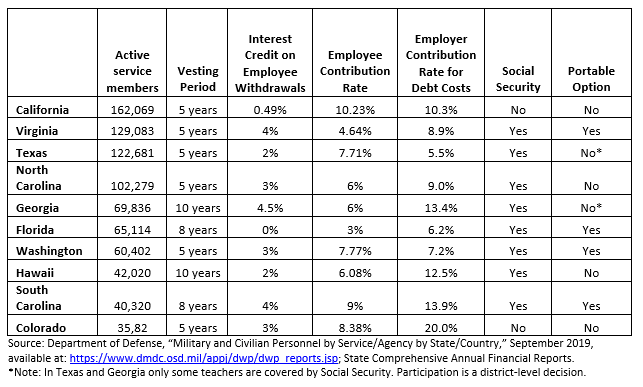

While there are military personnel in every state, the table below lists the ten states with the largest population of active duty military personnel. It also includes six elements of the state’s teacher retirement plan most relevant to military families. This piece will explore how these aspects of teacher pension plans affect military-connected families. How well they are served by these pension funds varies from state-to-state.

The first thing to notice is that each state has set a vesting period of at least five years. This means that an educator must teach at minimum for five years in the state to be eligible to receive the contributions to the pension fund the state made on her behalf. This presents a challenge to all educators, since in 30 states less than 50 percent of teachers ever vest in the system. This problem is particularly acute for military-connected families who move across state lines before reaching the years of service threshold required to qualify for benefits. In Georgia and Hawaii, teachers must work twice as long to qualify for a pension – far longer than a military family can expect to live in the same state. And given 70 percent of all active duty personnel are employed in these 10 states, it is likely that military families will be stationed in one or more of these states during their career.

For teachers who fail to vest in their state’s pension fund, how much they personally contribute each year is particularly relevant. The employee contribution rate -- the percentage of salary a teacher pays into the pension each year – can act like a forced savings mechanism, requiring teachers to put away some money each year for retirement. With this in mind, military-connected teachers tend to be better served by state plans with higher teacher contribution rates, such as in Colorado and Washington. Florida and Virginia, on the other hand, have relatively low contribution rates, which results in lower retirement savings for educators in those states. Additionally, the majority of states with the most active duty military personnel provide interest credit on a teacher’s own contributions if they leave the fund before vesting. For example, Virginia awards 4 percent interest on teacher contributions to those who exit prior to reaching the 5 year vesting threshold.

State spending on pension debt matters to all teachers. The more a state spends on debt costs – essentially playing catch-up on payments they missed in the past -- the fewer dollars they have available to be spent on benefits or increased teacher salaries. Greater spending on debt costs reduces a teacher’s total compensation, which is harmful generally, but most acutely for those educators who leave the state or the profession before qualifying for a pension.

Despite the challenges military-connected educators face with state pension systems, there is some good news: Six of these states participate in Social Security. This is critically important for all teachers, but especially those who move frequently from state-to-state since they can count on this monthly supplemental income when they retire. However, teachers who work all of their career in a state without Social Security will not receive those benefits in retirement. For teachers who move a lot, their time in those states will not count as qualified service for Social Security, and can reduce their benefit when they retire.

Another piece of good news is that four of the states with the most actively duty military personnel offer alternative, portable retirement plans. Like a typical 401k retirement plan, these plans can travel with teachers if they leave the state or the profession altogether. This can be a good option for educators who expect to move frequently.

Teacher pensions are designed for educators who spend their entire career in the classroom and in the same state. Simply put, these systems are ill-suited for military-connected families who are at risk of moving around the world. To better serve our service men and women and their families, states should consider providing them the option of enrolling in alternative retirement plans that are as mobile as they need to be.

Florida is the retirement capital for most of the United States. So at the very least the state’s own teachers and public workers should feel comfortable that they can retire comfortably there too some day. But that may not be the case.

Today’s Florida Retirement System has promised more than $30 billion in pensions than it has money to pay — and $15 billion of those are promised to K-12 educators. These “unfunded liabilities” have emerged only in the past 12 years and have been growing fast. If the current trends persist, it might be that the only people who can’t afford to retire in the Sunshine state are the people who served the state by teaching its children.

That’s why our team at Equable has launched FundMyFRS.org — and we are encouraging people to share with others about this troubling problem.

So what’s going on? In short, Florida is gambling away a secure retirement for teachers.

For years, market expectations for Florida pensions have been overly optimistic — leading to a massive miscalculation. Over the past two decades, FRS predicted even higher returns than what the record-breaking market brought in. It’s been so bad that over the past few years, even the advisors Florida has hired to help them manage pension finances have said FRS market expectations are unrealistic.

The result is that more than half of the $15 billion hole in pension funding for teachers is due to overly optimistic assumed rates of return.

To make things worse, the actual benefits that FRS is providing are increasingly not sufficient to ensure teachers get a secure retirement. Members of the Investment Plan do not have large enough contributions going into their accounts. Members of the Pension Plan are no longer earning benefits that will be inflation protected.

What can be done? There are a few things, but they will all require a stakeholders from across the state to join together and take on a big political challenge.

FRS needs a realistic assumed rate of return that Florida expects can be earned from financial markets. As it stands Florida is paying less today because it assumes it will earn more tomorrow. It would be better to have realistic expectations and put the money in today.

The Florida legislature needs to ensure it pays the full required contributions into the Pension Plan each year, and work to get the pension shortfall closed as quickly as possible.

Contributions into the FRS Investment Plan need to be increased so that there is more than the current 6.3% of salary being saved. Financial experts recommend that defined contribution plans get 10% to 15% of salary saved each year, in addition to Social Security.

Finally, the Florida legislature needs to ensure all retirement benefits are inflation protected, and find a way to re-introduce cost-of-living-adjustments to the benefits being earned by today’s public workers.

For more details visit FundMyFRS.org or check out some of the Florida posts here on TeacherPensions.org.

Anthony Randazzo is executive director at Equable Institute, a bipartisan non-profit working to create a safe, more secure retirement for public workers everywhere.

Teacher pension costs have been rising. Fast.

How do the rising costs of pensions affect other aspects of our education system? It’s relatively easy to point to simultaneous trends—for example, teacher salaries have been flat as pension costs have risen in recent years, and districts report that rising pension costs are leading them to cut back on other essential services.It’s much harder to draw a causal connection between fluctuations in pension costs and changes in the broader education system. There are a number of factors influencing school district budgeting decisions, and pensions are only one of many competing priorities.

However, a new study from Dongwoo Kim, Cory Koedel, and P. Brett Xiang attempts to disentangle these effects. I spoke with Koedel about their results. What follows is a lightly edited transcript of our conversation:

Aldeman: First, can you give a brief background on the paper. What questions were you trying to address?

Koedel: The paper is about where the money for pensions comes from. Pension costs have gone up a lot in recent years and following where that money is actually coming from is not easy. It’s not clear who is actually paying for the rising pension costs.

The purpose of our paper was to try to figure out one piece of that question. If some of the money to pay for pensions is coming out of teacher salaries (or not), that should be part of the political discourse about teacher pay and the teacher strikes that have been popping up.

For those who are unfamiliar with pensions, can you talk about how much teacher pensions cost and how that’s changed over time?

Pension costs have gone up pretty continuously since the turn of the century. Our data covers the years 2001 to 2015. During that time, the average annual required contribution went from about 12 to 22 percent of teacher salary. Our sample does not include all the states in the early years, but that’s a roughly accurate representation of the increase in costs nationwide.

A reason to think that teacher salaries might be affected is that pensions are collected as a percentage of salary. When districts and employees pay into the plan, they’re paying as a percentage of salary.

Plus, benefits are tied to salaries, so there’s a natural connection in the way that pension plans are funded and overall salary levels.

One thing you note in the paper is that pension costs are rising due to unfunded liabilities, not because benefit costs are increasing. Is that correct?

That’s right. The value of benefits is not increasing. The cost increases are predominantly from unfunded liabilities. I can’t say for certain that no state has improved benefits recently—though I don’t know of any—but a lot of states have reduced benefits. Of course, the benefit reductions only apply to new hires, so they take a while to phase in. But the bottom line is that benefits are not improving even as costs are rising.

What did you find? How are costs related to teacher salary expenditures?

We measured total teacher salary expenditures. You can think of teacher salaries as either going up on the extensive margin by expanding the number of employees, or on the intensive margin by raising the pay of the staff you already have. Our main analysis is inclusive of both of these margins. We are looking at the total salary bill and how that is influenced by changes in pension costs.

Prior to the Great Recession, we don’t find a relationship between pension cost fluctuations and salaries. It seems like these two aspects of compensation were acting independently.

However, since the Great Recession we do find an effect. Every 1 percent increase in the annual pension contribution has led to a reduction in total salary expenditures of .24 percent, on average.

We do our best to disentangle how salary expenditures are affected and the decrease seems to be driven by staff reductions (which could also include foregone staff expansions that would have happened in the absence of rising pension costs). Put another way, we don’t see average salaries going down. But we do see the total salary expenditure bill going down.

Can you hypothesize about why rising pension costs might hit staffing levels more than they would average salaries?

I’m totally speculating here because our analysis can’t speak to this directly. But there are mechanisms to help explain our results. It could be that in district negotiations with labor groups, it’s harder to negotiate salary reductions. I should be clear that a salary reduction here does not necessarily mean an outright cut in pay. We would detect an effect even if salaries were held flat or simply did not keep up with the increases that would have happened in the absence of rising pension costs. But we don’t see any movement on the average salary side, so a reasonable hypothesis is that labor negotiations are such that salaries are relatively protected, especially in contrast to decisions over staffing levels, and that’s where the cutbacks are happening. Districts have to pay for the pension costs somehow, and it seems like that’s the decision they are making.

Do you have any final thoughts or lessons for policymakers?

Our results point to something intuitive. Pension costs are going up fast, and we did find at least part of how they’re being paid for. That is, pension costs are leading to cuts in services in the form of reductions to the size of the teacher workforce.

My hope is that this will spark more interest in pensions from the education community. In the past, pension costs didn’t really affect this aspect of spending, but the world seems to have changed with the Great Recession. Pension costs are harming the bottom line in terms of delivering education services.

We ask a lot from teachers. We ask them to teach math, reading, and arithmetic, yes, and to be “nation builders” and instill civic virtues.

We also expect them to make incredibly complicated financial decisions about their retirement.

But wait, you might ask, aren’t most teachers covered by state-run pension plans that take care of retirement savings decisions? That is true, but most teachers won’t remain in those pension plans their full career. And when they leave, they’ll be faced with a difficult decision about what to do with their retirement money.

About half of all teachers won’t vest into their pension plan at all; they won’t be eligible for a pension from their pension system. These teachers are eligible to withdraw their own contributions, sometimes with a small amount of interest, but only two states provide exiting teachers with any employer contributions. These teachers need to decide whether they should keep their money in the pension plan, or whether they're better off withdrawing their money and rolling over their savings into an Individual Retirement Account (IRA).

That’s a tough decision, particularly if the teacher is simply taking time off to start a family or is thinking about returning at some point in the future. But it’s nowhere near as tough as the decision faced by teachers who are vested.

A vested teacher will qualify for a pension upon retirement, but that may be many years away, and their future pension will be based on their salary today, unadjusted for inflation. What is the pension worth today, in real, inflation-adjusted dollars? That’s a much tougher calculation, and it depends on how fast you think inflation and investments will grow over time. Smart economists have different answers to these questions, so what’s a teacher to do?

According to a recent study on the behavior of Illinois teachers, most teachers take the conservative route of inaction. Looking across all departing, vested teachers, 73 percent opt to leave their money with the pension plan. That means about one-quarter of vested teachers withdraw their contributions. All together, in addition to the 62 percent of teachers who won’t vest in Illinois, that means roughly three-fourths of Illinois teachers will either fail to qualify or choose not to receive a pension. Those rates vary somewhat by type of teacher. Males are more likely than females to withdraw their money. Hispanic and, especially, black, teachers are more likely to withdraw than white teachers.

But are these teachers making the “right” financial decision? That depends, again, on their personal situation and how fast they might be able to grow their investments on their own.

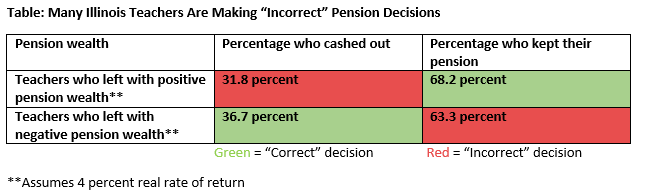

In the Illinois study, economist Martin Lueken calculated the net pension wealth for every teacher based on their age and years of experience. If teachers had an expected pension wealth above what they would have been able to withdraw and invest on their own, he considered them to have a “positive” net pension wealth. If not, he classified them as having a “negative” net pension wealth. Then, he adjusted their net pension wealth based on potential investment returns. The higher the investment return teachers could earn themselves, the less likely they were to have a positive net pension wealth (that is, the better they were at investing on their own, the less valuable the pension amount became).

If teachers could take their own money and earn an investment of only 2 percent above inflation, just 14 percent of vested Illinois teachers would leave with a negative pension wealth. That's a very modest assumption, and most teachers would be better off leaving their money with the pension plan in that circumstance. But if teachers could do a little better with their investments and earn a 4 percent return (still not an outrageous assumption), then 73 percent of teachers would leave with negative pension wealth. They would be better off pulling their money than leaving it in the pension plan. (At 6 percent, a high investment return but still below what the state itself thinks it can earn, 88 percent of teachers would be better off pulling their money.)

For each of these scenarios, Lueken’s calculations allow us to see how many teachers made “correct” or “incorrect” financial decisions*. Depending on the assumed investment return, somewhere between 32 and 64 percent of teachers were making incorrect decisions. The chart below illustrates where teachers would fall under the 4 percent assumption. In this moderate scenario, more than half of all departing teachers are making the wrong decision. About 32 percent of teachers with positive pension wealth cashed out but shouldn’t have, and 63 percent of teachers with negative pension wealth should have cashed out but didn’t.

Teachers are well-educated, intelligent people, but to make these decisions requires a lot of foresight and willingness to deal with uncertainty. Pension plans are essentially asking teachers to predict whether they’ll return to teaching and to compare their pension wealth, in future dollars, versus how much it might be worth if they invested their money elsewhere. That’s complicated stuff, and it’s something most teachers don’t have the time to contemplate.

In comparison, most workers in the private sector have much easier decisions. Unlike under a pension plan, they have to decide their own investments, but they're given a limited list of options. Increasingly, private-sector employers are nudging workers into making good decisions. And, when they leave a job, the choices are simpler. They can either leave their money in the existing funds, or roll it over to IRAs. The questions for private-sector workers are really about investment options and fees, and they’re much more straightforward than the decisions teachers face.

States, on the other hand, systematically force public school teachers to make extremely complex financial decisions. Saving for retirement is hard enough; we shouldn't force teachers into such complex decisions.

*"Correct" in this context is hypothetical, based purely from a financial standpoint, and it assumes teachers had full information about the value of their pensions. In real life, individual teachers don’t have perfect information and must weigh trade-offs from their own unique perspective. As with all of our work here at TeacherPensions.org, this post is illustrating public policy choices and is not intended as personal investment advice. Teachers should consult a qualified financial professional before making consequential financial decisions.