We ask a lot from teachers. We ask them to teach math, reading, and arithmetic, yes, and to be “nation builders” and instill civic virtues.

We also expect them to make incredibly complicated financial decisions about their retirement.

But wait, you might ask, aren’t most teachers covered by state-run pension plans that take care of retirement savings decisions? That is true, but most teachers won’t remain in those pension plans their full career. And when they leave, they’ll be faced with a difficult decision about what to do with their retirement money.

About half of all teachers won’t vest into their pension plan at all; they won’t be eligible for a pension from their pension system. These teachers are eligible to withdraw their own contributions, sometimes with a small amount of interest, but only two states provide exiting teachers with any employer contributions. These teachers need to decide whether they should keep their money in the pension plan, or whether they're better off withdrawing their money and rolling over their savings into an Individual Retirement Account (IRA).

That’s a tough decision, particularly if the teacher is simply taking time off to start a family or is thinking about returning at some point in the future. But it’s nowhere near as tough as the decision faced by teachers who are vested.

A vested teacher will qualify for a pension upon retirement, but that may be many years away, and their future pension will be based on their salary today, unadjusted for inflation. What is the pension worth today, in real, inflation-adjusted dollars? That’s a much tougher calculation, and it depends on how fast you think inflation and investments will grow over time. Smart economists have different answers to these questions, so what’s a teacher to do?

According to a recent study on the behavior of Illinois teachers, most teachers take the conservative route of inaction. Looking across all departing, vested teachers, 73 percent opt to leave their money with the pension plan. That means about one-quarter of vested teachers withdraw their contributions. All together, in addition to the 62 percent of teachers who won’t vest in Illinois, that means roughly three-fourths of Illinois teachers will either fail to qualify or choose not to receive a pension. Those rates vary somewhat by type of teacher. Males are more likely than females to withdraw their money. Hispanic and, especially, black, teachers are more likely to withdraw than white teachers.

But are these teachers making the “right” financial decision? That depends, again, on their personal situation and how fast they might be able to grow their investments on their own.

In the Illinois study, economist Martin Lueken calculated the net pension wealth for every teacher based on their age and years of experience. If teachers had an expected pension wealth above what they would have been able to withdraw and invest on their own, he considered them to have a “positive” net pension wealth. If not, he classified them as having a “negative” net pension wealth. Then, he adjusted their net pension wealth based on potential investment returns. The higher the investment return teachers could earn themselves, the less likely they were to have a positive net pension wealth (that is, the better they were at investing on their own, the less valuable the pension amount became).

If teachers could take their own money and earn an investment of only 2 percent above inflation, just 14 percent of vested Illinois teachers would leave with a negative pension wealth. That's a very modest assumption, and most teachers would be better off leaving their money with the pension plan in that circumstance. But if teachers could do a little better with their investments and earn a 4 percent return (still not an outrageous assumption), then 73 percent of teachers would leave with negative pension wealth. They would be better off pulling their money than leaving it in the pension plan. (At 6 percent, a high investment return but still below what the state itself thinks it can earn, 88 percent of teachers would be better off pulling their money.)

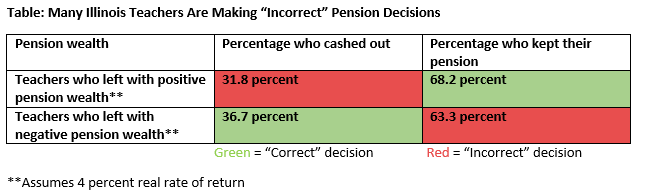

For each of these scenarios, Lueken’s calculations allow us to see how many teachers made “correct” or “incorrect” financial decisions*. Depending on the assumed investment return, somewhere between 32 and 64 percent of teachers were making incorrect decisions. The chart below illustrates where teachers would fall under the 4 percent assumption. In this moderate scenario, more than half of all departing teachers are making the wrong decision. About 32 percent of teachers with positive pension wealth cashed out but shouldn’t have, and 63 percent of teachers with negative pension wealth should have cashed out but didn’t.

Teachers are well-educated, intelligent people, but to make these decisions requires a lot of foresight and willingness to deal with uncertainty. Pension plans are essentially asking teachers to predict whether they’ll return to teaching and to compare their pension wealth, in future dollars, versus how much it might be worth if they invested their money elsewhere. That’s complicated stuff, and it’s something most teachers don’t have the time to contemplate.

In comparison, most workers in the private sector have much easier decisions. Unlike under a pension plan, they have to decide their own investments, but they're given a limited list of options. Increasingly, private-sector employers are nudging workers into making good decisions. And, when they leave a job, the choices are simpler. They can either leave their money in the existing funds, or roll it over to IRAs. The questions for private-sector workers are really about investment options and fees, and they’re much more straightforward than the decisions teachers face.

States, on the other hand, systematically force public school teachers to make extremely complex financial decisions. Saving for retirement is hard enough; we shouldn't force teachers into such complex decisions.

*"Correct" in this context is hypothetical, based purely from a financial standpoint, and it assumes teachers had full information about the value of their pensions. In real life, individual teachers don’t have perfect information and must weigh trade-offs from their own unique perspective. As with all of our work here at TeacherPensions.org, this post is illustrating public policy choices and is not intended as personal investment advice. Teachers should consult a qualified financial professional before making consequential financial decisions.