A version of this article first appeared last year in The 74.

September means that football is finally here! After months of waiting, the new NFL season kicks-off tonight. I've got my fantasy football lineups (yes multiple) all set and I've thoroughly convinced myself -- at least for one week -- that the Buffalo Bills have a chance to be in the playoff hunt. September is a time of hope not only for NFL playes and fans, but also for students and teachers as a new school year begins.

Teachers and NFL players have more in common that you might at first realize. Both in the NFL and in classrooms, rookies abound. We rely on rookie teachers more than in the past. In the NFL, more than 200 rookies joined the league in April. The commonalities don’t stop there. Neither teachers nor NFL players can expect to stay in their profession for very long. And, surprisingly, both teachers and NFL players are among the very few careers that offer a pension for retirement.The problem is that the pension system really isn’t very good for either.In the NFL, players now need five years of service before they vest and become eligible for a pension. In the world of pensions, that is a reasonable vesting period. But the devil is in the details: Most players don’t stay in the league long enough to qualify. The average career lasts only 3.3 years. The NFL disputes this figure and instead claims that for players who make a team’s 53-man roster as a rookie, the average career is 6.86 years.Based on these estimates, it’s reasonable to conclude that around half of all NFL players never earn a pension. Among those who do qualify, the average pension was worth $43,000 per year in 2014. They can begin to draw on their pension at age 55.It’s about the same for teachers. Around half leave the profession without a pension. But in 21 states, the vesting period is longer. And in 15 states, teachers need to work at least twice as long as NFL players to be eligible for a pension. Like NFL players, most teachers do not stay long enough, so when their teaching careers end, often they walk away with no retirement savings. To make matters worse, for those educators who do stay long enough to be eligible for a pension, it will take about 22 years to break evenon their contributions.In other words, for most teachers, their individual contributions to their pension are more valuable than the pension itself until they teach for more than 20 years.So for those of us keeping score, most teachers and NFL players are ineligible for a pension. But the NFL scores points because football players typically earn a pension that is more valuable than the average teacher pension in 46 states. And they are able to collect their retirement funds at an earlier age than most teachers.While the pension plan for the NFL does not serve its players particularly well, teachers fall far short of the goal line when it comes to their retirement. Here are the top six ways that teacher pensions are outperformed by the NFL pension plan:- Money, money, money! Football players earn, at minimum, hundreds of thousands dollars more than teachers. Although the value of an NFL player’s pension does not depend on his salary, it does for teachers. So that means teachers need to work for decades and seek out the highest salary possible in their final years to maximize their retirement benefit.

- Social Security woes. Social Security is for everyone, right? Wrong. It is for football players. But in several states, teachers cannot participate in Social Security. In fact, about 1.2 million teachers are not covered by Social Security. Not only does this mean less money when they retire, it can also leave teachers particularly vulnerable to poorly designed pension plans.

- You can take your money with you. NFL players move around a lot. Even the Sheriff, Peyton Manning, one of the biggest winners from the NFL pension system, had to move once. Moving doesn’t affect their retirement funds. It makes sense that they can take their money with them. But this is not true for teachers. Their retirement benefits, even if they are vested, are not portable. That means any teacher who moves out of state has to leave that retirement fund there and start a new one in their new state. Keeping two pension plans can amount to hundreds of thousands of dollars in losses.

- Choices. NFL players have the option of opening a 401(k) account with the league in addition to their pension. In fact, the plan is really generous. The league will match player contributions at a 2-to-1 rate for up to $26,000. Most teachers have access to a portable retirement plan, but they rarely receive matching contributions from their employers.

- The NFL is a lucrative and stable employer. The NFL is at least a $45 billion industry with more than 12,000 current and former players. It’s in great shape. Players don’t have to worry – at least not seriously – that the league will go bankrupt or suddenly decide not to fund its pension. Teachers aren’t so lucky. Many states kicked the can for decades and now have billions of dollars of unfunded pension liabilities. In Chicago, home of the Bears, the district is estimated to be about $20 billion behind. To make matters worse, teacher pension funding is handled by ever-changing state legislatures. One year they might get policy makers who meet their pension obligations. The next year, they might not. Yikes.

- Teachers are vilified, while football players are idolized. Even though Comedy Central’s Key and Peele did a great teacher “mock draft,” I doubt anyone has a Fat Head poster of a teacher. The simple truth is that NFL players are revered. In Boston, Tom Brady can do no wrong. It’s pretty much the opposite for teachers. They’re called glorified babysitters; New Jersey Governor Chris Christie threatened to punch them; and they’re blamed for state fiscal woes.

So let’s recap: Neither NFL players nor teachers have a pension plan that meets the majority of their needs. But for teachers, the failure of the plan to provide a good retirement benefit is particularly costly.To fix this, states have got to stop the bleeding. They need to, at a minimum, offer teachers a pension that provides retirement security for all, or a portable retirement account with a savings match. This wouldn’t eliminate states’ current liabilities, but it would make sure that they don’t dig the hole any deeper. And, as any good football fan knows, when you’re down, the comeback starts with defense.A version of this article first appeared last year in The 74.

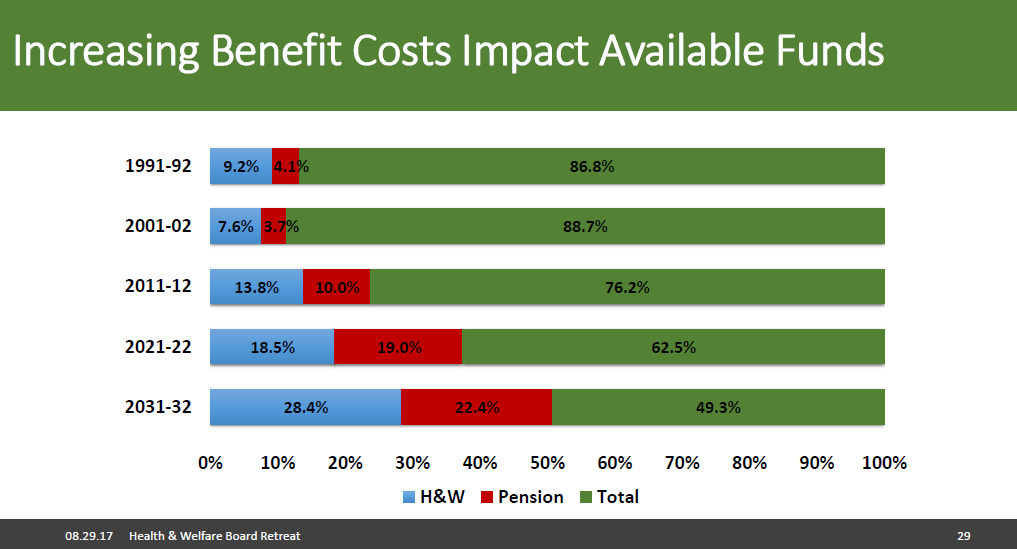

Want to see the future of school district budgets? Take a look at a slide deck presented this week by the Chief Financial Officer of the Los Angeles Unified School District (hat tip to reporter Kyle Stokes). The presentation was primarily about the rising cost of healthcare and post-employment benefits, but it included this alarming slide:

As shown in the graph, Health and Welfare (labeled “H & W” in the graph) benefits consumed 9.2 percent of the district’s budget in the 1991 school year. By 2021, they are projected to consume 18.5 percent of the district’s budget, rising to 28.4 percent by 2031. Pensions are similar: Los Angeles devoted 4.1 percent of its budget toward pensions 1991, but that will rise to 19 percent in 2021, and rise again to 22.4 percent by 2031.

Los Angeles is now considering a range of cost saving “opportunities,” primarily on the healthcare side, but assuming no policy changes, benefit costs for current workers and retirees will eat up more than half of L.A.’s budget by the year 2031.

As we’ve written before, this is a national trend, and it’s not a good one. It will compress teacher salaries and mean less money for books, field trips, libraries, foreign language, after-school programs, pre-k, etc. Like the Pac-Man game, benefit costs are steadily eating into the budget for everything else we care about in schools.

Taxonomy:Money spent on public teacher pensions is often left out of analyses of school finance equity. Rather than a being seen as an issue affecting students’ education, pensions are often viewed as a budgetary dilemma for state legislators. Yet, both of these approaches overlook the effect pension spending can have on increasing the funding gap between schools based on students’ race.

Last week I released a new report, “Illinois’ Teacher Pension Plans Deepen School Funding Inequities,” that shows just how much pension spending in Illinois affects the state's finance equity. The results are startling and reveal that teacher pensions are yet another example of how states and districts underinvest in the education of low-income students, and the educations of black and Hispanic students.

Here are three key reasons why teacher pensions should be thought of as a key part of the push to ensure educational equity:

- Class-based gaps grow by more than 200 percent after accounting for pension spending. Teacher salaries comprise the lion’s share (roughly 80 percent) of school expenditures. And, unfortunately, the most experienced and highest paid teachers are unevenly distributed across schools. In Illinois the salary gap between the schools serving the highest and lowest concentrations of low-income students is on average around $550 per pupil. After factoring in pensions, however, the disparity jumps to over $1,200 per student.

- Race-based gaps increase by more than 250 percent after accounting for pension spending. In Illinois, the average teacher salary-based gap is $375 between schools serving predominantly white students and those serving predominantly nonwhite students. But after accounting for money spent on teacher pensions, the inequity increases to nearly $950 per pupil.

- States are investing more money in their pensions (because they’re in significant debt), and that will widen the gaps even further. From an educational equity point of view, the Illinois pension system is the problem. Since pensions are paid as a percentage of teachers’ salaries, which are unevenly distributed across the state, funneling more money into the system may help to decrease unfunded liabilities, but it also will result in even larger funding disparities.

Illinois is widely considered to operate one of, if not the most, inequitable school finance system in the country. Yet, many prior analyses underestimated the problem because they have not always included money spent on teacher pensions. This problem is not unique to Illinois. On the contrary, pensions will increase funding disparities in any state with an uneven distribution of teachers. The effect will likely be greater and more closely resemble Illinois in states, such as Missouri and New York, where large urban cities operate separate pension funds.

There are a couple of steps states can take to mitigate the increase in education funding disparities due to pension spending. Those states with more than one retirement system should consider folding the district plans into the state fund. The state has greater resources and almost always contributes to the pension fund at a higher rate. This would ensure that schools in the district — which disproportionately serve low-income students and students of color — receive pension payments at the same rate as other schools.

As it stands now, low-income students and students of color receive far less than their fair share in school funding. To change that, states must address the structure of their teacher pension systems as well as their school funding formulas. Teacher pensions are a key feature in the broader education equity debate.

Pensions are for survivors.

That's the first thing that struck me when reading the National Public Pension Coalition (NPPC) short report, “Why Pensions Matter: The history of defined benefit pension plans in the United States of America.” It starts out like this:

Pensions, in the broadest sense of the term, have existed since ancient Rome. Soldiers in the Roman army could earn pensions through their military service. The value of these pensions to Roman soldiers helped to maintain the power of emperors such as Augustus. Pensions for military service have continued to exist in one form or another in the two thousand years since.

This is true as far as the history goes, but it’s a telling anecdote, because it's a reminder that pensions benefit survivors. In the past, that meant surviving war. Today, that means remaining in one profession and one state for an entire career. State pension plans assume that less than one-in-five teachers will survive long enough to truly benefit from today’s back-loaded teacher pension plans.

The report is a few months old now, and it has some useful historical notes, but it also includes a number of attempts to gloss over the true history of retirement savings in this country. To show where the NPPC's history bleeds into a false nostalgia, I’ve pulled out a few sections below and annotated where the report goes wrong:

During the postwar economic boom, defined benefit pensions represented the closing chapter of a solid middle class life. The American dream was a steady job with a middle class salary, decent benefits, and the promise of a pension in retirement. For many, but not all, Americans this dream was a reality. A worker with a high school education could get a job on the line at a steel factory and live that middle class lifestyle. Other workers found job security and a good salary through serving their community as a teacher or firefighter or librarian. For a period of time, pensions were accepted as a key element of middle class life in the United States. This started to change in the 1980s.

The words "promise," “dream,” and “could” are doing a lot of work here. As I’ve written before, it’s a myth that there was ever some sort of “golden era” where all workers had access to a secure retirement. In the early 1980s, only 43 percent of new retirees had any retirement benefits other than Social Security. That was before pensions began to decline and the 401k began its steady ascent, and yet most Americans still did not have any retirement benefits.

Moreover, retirement income was highly contingent on income. During the peak era for defined benefit pension plans, only 22 percent of retirees in the bottom quartile had any retirement income other than Social Security, compared to 64 percent among those in the highest quartile.

In other words, while it was theoretically possible for anyone to graduate high school and earn a factory job with a pension, there just weren’t that many people who were able to take advantage of that dream. There are lots of reasons for this—there weren’t that many factory jobs to go around, those pensions required long vesting periods of 10 or 20 years, and lower-income workers have higher turnover rates—but suffice it to say that the NPPC’s history is overly rosy on this front.

They go on:

Critics of public pensions often complain that these pension plans have long vesting periods and reward the longest serving employees. That is intentional. In public education, for example, most research points to teachers dramatically increasing their effectiveness during their first few years of teaching and then maintaining that effectiveness throughout their career. They do not lose their effectiveness the longer they continue in their profession. They are more likely to continue teaching at their peak effectiveness rather than decline. Structuring retirement plans to reward teachers that only teach for three or four years does not make sense because that would reward teachers who leave before reaching their peak effectiveness, often to be replaced by someone without any experience. Similarly, with firefighting and policing, there are a lot of sunk costs that go into training new recruits. It is not in the interest of these departments for their new employees to leave right after training, so their pension plans are structured to promote long-term commitment to the profession.

It’s noteworthy to see a union-backed coalition like the NPPC make their priorities this explicit. They’re essentially admitting that they only care about retirement security for those “committed” to the profession. But, because pensions don’t provide positive benefits to teachers until they’ve served for 20 or 25 years, the NPPC’s definition of “commitment” excludes the majority of people of people who enter the teaching profession. To extend the metaphor, they really only care about the survivors in a war of attrition. They’re also overstating the teacher effectiveness research a bit, but, regardless, as a matter of public policy affecting millions of workers, we should work to ensure they ALL have retirement security.

Later they state:

State and local governments offer defined benefit pensions to their employees in order to attract the best and brightest to public service. Public employees earn less on average than their counterparts in the private sector, so job benefits like pensions are a proven way to recruit top talent. Also, as discussed above, pensions play a key role in retaining employees in professions like teaching and firefighting.

This claim is not backed by research. To begin with, we don’t have good evidence on how much pensions affect teacher recruitment. Some teachers might choose to teach because of the promise of a pension, but the long wait for a decent pension also might deter some qualified candidates. Moreover, extremely high (and rising) pension costs have played a role in keeping teacher salaries flat in recent years, and those costs have also contributed to large cuts in pension benefits for new teachers.

We do, however, have evidence on pensions as a retention incentive, and it's not nearly as positive as the NPPC claims. As Kelly Robson and I showed in a recent report for Education Next, state pension plans themselves do not assume that qualifying for a pension is enough to alter teacher behavior. At the back end, pensions do have a retention effect on teachers nearing retirement age, but that comes too late to affect teacher retention rates very much. Moreover, if we care about keeping veteran teachers, then we should be concerned about the much larger “push-out” effect that pensions have on teachers who reach the normal retirement age.

Later they revisit the broader argument about retirement security:

In the private sector, the shift from defined benefit pensions to defined contribution 401(k) plans over the past three decades has harmed the retirement security of working families. This is because most working families accumulate far less in retirement savings with a defined contribution plan than they would with a defined benefit pension.

This claim seems like it could be true, but it's not. As discussed above, there was no golden era of retirement saving. In fact, researchers have looked at multiple sources of data and found that today’s retirees are doing at least as well, if not better, than prior generations. (Lest you think anyone is cherry-picking data, the links in the prior sentence will take you to work published by the U.S. Census Bureau, the conservative National Affairs magazine, and the left-leaning Mother Jones.)

That doesn’t mean problems don’t exist—about half of all workers today still do not have access to a retirement plan at their jobs—but pension advocates are seizing on the problems of today in order to make a case for a past that never existed in the first place. It's understandable that as a trade group representing large pension plans, the NPPC doesn't want to have a conversation about why public-sector retirement plans like those offered to teachers are getting worse over time, while those offered in the private sector keep getting better. But that would be a more complete reading of the history.

Taxonomy:Tomorrow will be July 1st. For teachers that means summer school, prep for next year, and some well-deserved time off. For Major League Baseball fans, July 1st is Bobby Bonilla day. For any non-baseball fanatics out there, Bonilla remains famous not for his playing career, which ended in 2001, but for an odd deferred-money contract the New York Mets gave him in 2000. Instead of paying him roughly $6 million at the time, the Mets instead offered to pay him in yearly installments, paid out on July 1st every year from 2011 until 2033. In short, the club offered him something very similar to a pension.

Even though Bonilla was getting paid in the millions, his story relates to millions of teachers: In most cases a pension might not be worth it over the long run.

Let's unpack this comparison a little further.

In 2000, the Mets wanted to save some cash, so they delayed Bonilla's salary. In exchange Bonilla would receive a much greater, albeit delayed, sum. It seemed like a win-win. The club was deeply invested with Bernie Madoff and they (incorrectly) assumed that they would earn good returns in the market. Many pension funds make the same mistake. Nevertheless, the Mets were after much-needed financial wiggle room to make payroll, and giving Bonilla a contract worth more than a player of his caliber and age might have otherwise demanded seemed prudent at the time.

Teacher pensions are a lot like Bonilla’s deal.

Nearly all teachers receive a pension, also known as defined benefit (DB) retirement plan. Here is how it works. States and often districts pay a percentage of a teacher’s salary into a pension fund. Teachers also are required to make an annual contribution. At retirement teachers receive annual benefits according to a formula based on their age, years of experience, and an average of their final salaries.

Like the Bonilla arrangement, teachers forgo higher salaries today in exchange for more lucrative benefits tomorrow. This approach reduces how much money states need to pay in salaries and provides teachers with the opportunity to make up, and maybe even exceed, the difference later through the pension fund. A win-win, right?

Unfortunately, however, neither Bonilla nor teachers made out as well financially as one might have guessed. According to an estimate by ESPN last Bonilla Day, had he taken the money upfront and invested it, even with a conservative rate of return, he would have made more money. And for the Mets, they're still paying a retired 50 year-old over $1 million a year.

Most teachers get a raw deal as well. In the current pension system it takes teachers on average 24 years to earn a pension as valuable as the money they invested themselves. Many teaches would be better off financially if they could take their pension payments as salary. Or alternatively, a defined-contribution (DC) plan such as a 401k plan would produce a more valuable retirement benefit for most teachers.

The news isn't any better for states. Nationally, states carry around half a trillion dollars in unfunded liabilities. Pension funds in Puerto Rico and states such as Illinois and New Jersey face bankruptcy if they don't reform their systems.

The truth is that Bonilla, bad deal aside, will very likely be fine financially. For millions of teachers, however, it is a different ball game.

All teachers deserve a secure retirement. But under today’s current teacher retirement savings plans, more than half of all new educators won’t qualify for even a minimal pension benefit. We took a state-by-state look at public teacher retirement plans, and the findings were dismal. Here’s what we saw:

Retirement plans for public-sector workers, including teachers, are, by and large, getting worse. The last recession came down hard on state governments; so much so that, in terms of retirement benefits, now is the worst time in at least three decades to become a teacher. Those cuts fall hardest on new and future teachers, particularly those who do not plan teach in the same state for their entire careers. Our rankings aimed to capture these discrepancies, highlight areas of progress, and provide recommendations for reform.

We didn’t pull any punches – the reality of the situation is bleak, and it is important to share the facts. The majority of states are enrolling their teachers in expensive, debt-ridden retirement systems that fail to provide most teachers with adequate savings. These plans are unfair and unsound. We also aren’t the first to champion for pension reform. The Urban Institute has an excellent resource on public pensions, and our report draws on data from the National Council on Teacher Quality, in partnership with EducationCouncil. Our rankings build on these efforts in an important way, by adding in details to reflect the key differences between states. Teachers in California may have different needs than those in Idaho; these states may need to implement different policies to meet these needs. We believe states should design retirement plans that support their particular teacher workforce.

To measure the extent to which states have created retirement systems that match and adequately support their existing teachers, we created a grading rubric focused on two questions: 1. Are all of the state’s teachers earning sufficient retirement benefits? And 2. Can teachers take their retirement benefits with them no matter where life takes them? Our rankings use an equally weighted grading system comprising six variables that help answer our two guiding questions. Those variables are:

- The percentage of teacher salaries going toward retirement

- The percentage of teacher contributions going toward pension debt

- The percentage of teachers who qualify for employer-provided retirement benefits.

- The percentage of teachers who earn retirement savings worth at least their own contributions plus interest

- The percentage of teachers covered by Social Security

- Whether or not a portable retirement savings option exists

Our rankings paint a sobering picture. No state scored higher than a C, and most came in at an F. Overall, while states tend to be contributing enough toward benefits, they haven’t managed debt well or ensured that all teachers have access to adequate retirement savings. Few states have adopted reforms that would give teachers portable retirement benefits with the freedom of mobility or other personal or career choices. Others do not offer Social Security coverage to their teachers, depriving them of a solid base of retirement savings. It’s also important to note that just because a state has managed its debt costs reasonably well does not necessarily mean its plan is working well for teachers.

New York is one such example. The state does okay overall in our rankings, coming in ninth. Debt costs are low, but the state requires new teachers to stay 10 years before qualifying for retirement benefits. This leaves 60 percent of the state’s teacher workforce without any pension benefit at all. Similarly, Wisconsin has debt costs of just 1 percent of teacher salaries, but teachers are left out of Social Security coverage and must stay in the classroom 21 years before they break even on their own contributions plus interest. Both states have managed their finances reasonably well, but neither one is truly meeting the retirement needs of their teacher workforces. In fact, they’re managing their pension finances on the backs of teachers, at least in part, by perpetuating heavily back-loaded systems that reward a few at the expense of most teachers.

Something needs to change. Our teachers deserve better, and while specific action steps will vary state-to-state, we believe all states should aim to provide all their teachers with a secure retirement. They can start by:

1. Getting their finances under control

2. Making portable teacher retirement plans the default, to provide all teachers with financially secure benefits

3. Expanding Social Security coverage to include teachers

Curious about your state? Click here to see where it stands, or see the report for a breakdown of our overall rankings.