After spotting a deal that looked too good to pass up, you discover a flaw and end up returning and getting a refund on your purchase. It may sound shocking and counterintuitive, but in many cases, teachers may actually be in a similar situation with their pension plans. They might be better off taking a refund on their contributions rather than waiting around to receive a pension.

How is this possible? Teachers qualify for very little in the way of retirement benefits during the first half of their career because pension benefits don’t accrue evenly. A mid-career teacher therefore is faced with a choice: she qualifies for some pension and can receive lifelong payments upon retirement, or she can forfeit her rights and get a refund on her contributions.

New research from the Urban Institute compares the value of a teacher’s contributions to a teacher’s overall pension wealth. Using the pension plan’s own interest assumptions (often 8 percent), in half of states teachers need to stay in a single system for at least 24 years to simply break even on their contributions plus interest. Even using a more conservative 5 percent interest rate, a teacher would need to stay for at least 15 years in order to break even in the median state. This means that an individual teacher could work for over a decade, diligently contributing to the system, and qualify for a pension that’s worth less than the value of her own contributions plus interest. She may actually lose money to the state pension system.

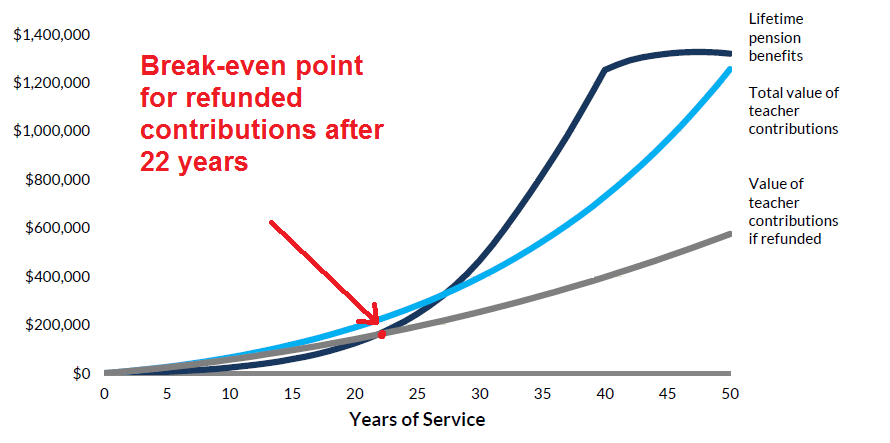

The graph below shows the differences in the value of a newly hired, 25-year-old California teacher’s lifetime pension benefits, her contributions using the plan’s interest assumptions (7.5 percent interest), and her contributions if the teacher requested a refund. Although California assumes it can earn 7.5 percent interest every year on the plan’s assets, the state plan only gives teachers 4.5 percent interest on refunded contributions. For a new California teacher, even the limited refund policy would be worth more than her actual lifetime pension benefits for the first 22 years of her career. She would be better off getting a refund and giving up the pension if she teaches for anything less than 22 years.

The Value of a Teacher's Contributions Versus Future Benefits

Source: Richard Johnson and Benjamin Southgate, “Can California Teacher Pensions Be Distributed More Fairly,” Urban Institute, October 2014.

Refunding and rolling over her contributions to a tax-sheltered savings vehicle would actually allow that teacher to grow and invest her contributions, rather than giving it up to the state and waiting the years before she can actually collect a retirement pension, whereupon its value has eroded over time. Most state pension formulas, including California’s, don’t adjust salary figures for inflation when calculating benefits. A teacher, of course, has to weigh the risks and her own savings habits; if she is prone to high spending or making risky purchases where she burns through all her contribution money rather than saving, otherwise known as “leakage,” then keeping it locked away with the state in exchange for a small pension down the road may be a better decision.

On the surface, a lifelong annuity sounds like a great deal. In California, the plan assumes that less than a quarter of teachers with 15 years of experience will take a refund. In other words, the plan assumes that most teachers who qualify for a pension usually take it. But not all pensions are equal, and for many teachers, pensions likely carry a flaw that demands a refund. The reality is that pensions vary vastly depending on how many years of service a teacher has and when she can actually retire and collect. Just because a teacher has the option to get a pension at some point down the road doesn’t necessarily mean she should take it.

*This is post is based on research on California’s teacher retirement plan. It is not personal or institutional investment advice. Please consult a qualified financial professional before making consequential financial decisions.