Earlier this month the Democrats on the Joint Economic Committee issued a report called “Retirement Security in Peril.” While they get some facts right, they also miss the forest for the trees. Worse, the story they tell about the retirement security offered to our nation’s public school teachers is dangerously wrong. Instead of praising those plans, congressional Democrats should be doing more to protect this large and important group of workers.

First, it’s true that many American workers lack any retirement savings at all, and there’s been a shift in the private sector away from defined benefit plans to defined contribution plans. This shift has put more of a burden on workers to save on their own, rather than relying on their employer.

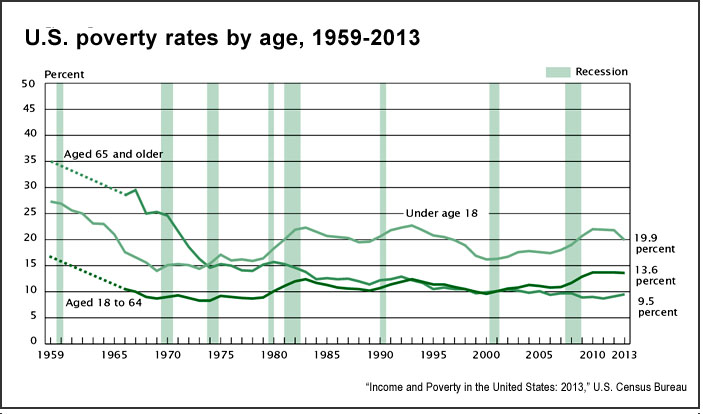

But contrary to the narrative put forward in the report, these shifts haven’t harmed our collective retirement prospects. If the congressional Democrats had read a recent report put out by the U.S. Census Bureau, they’d recognize that our reduction in old-age poverty is one of our greatest accomplishments over the last few generations. Through safety net programs like Social Security and Medicare, as well as private savings that have proven surprisingly resilient, we’ve significantly reduced poverty rates among the elderly. Contrary to the “peril” described in the Democrats’ report, elderly Americans are less likely to be poor than any other age group.

{kind=link}

Democrats should be playing the role as vigilant watchguards of this progress, but that will require them to diagnose our true challenges more accurately. For example, rather than generic calls for “expanding” Social Security, we should be talking about how to make the Social Security formula more progressive to better cover low-income Americans with spotty work records and limited access to retirement savings plans.

Moreover, the report’s descriptions about teacher pension plans are wildly out of touch with reality and attempt to paper over real problems in the public sector. Here’s what they write:

Teacher pension plans are an example of the key role that defined benefit plans play in providing families a stable retirement. Teacher pensions, much like other defined benefit plans, provide a more secure path to retirement, helping many teachers overcome the multitude of obstacles that prevent saving for retirement. More than 75 percent of teachers participate in defined benefit plan. These pension plans reward longevity with an employer, creating economic incentives for high-quality teachers to stay in the profession. These plans serve as effective recruitment and retention tools for schools, helping attract and maintain the best teachers to ensure student success. Pension plans also afford teachers a more predictable source of income into retirement, which is particularly important for low- and middle-income teachers.

This is little more than teachers’ union talking points, and it ignores a large and growing body of work about the problems with teacher pension plans. Here’s the truth:

- Teacher pension plans do work well for certain groups of teachers who stay in the profession for their entire career. But that’s only a small fraction of the workforce. Depending on the state, two-thirds to three-quarters of teachers don’t stay long enough to benefit from the pension system. Congressional Democrats should care about these people.

- Teacher pensions reward longevity within a state (not any particular employer), but the rewards are so difficult to understand and occur so late in a teacher’s career that few teachers react to them. When we looked at early-career teachers, we found that teachers will not put in even a single extra year to qualify for a pension benefit. A study looking at a costly pension enhancement in St. Louis found it only affected the behavior of a very small group of teachers who were right on the cusp of retirement. Another study out of Oregon also failed to find any effect.

- Unlike in the private sector, where Congress has taken steps to improve the benefits offered to workers and the funding stability of their retirement plans, public-sector plans lack those same basic protections, and the plans have adopted unnecessarily risky actuarial assumptions. For example, 15 states require teachers to serve for 10 years before qualifying for retirement benefits, which would be illegal in the private sector. Virtually every state-run teacher pension plan would fail the financial rules that Congress put in place to protect workers in private-sector plans.

- States have managed their teacher pension plans so poorly that they’re now under-funded by $500 billion. Due to rising costs, states have dramatically cut retirement benefits for new workers, and states and districts have been forced to scale back their spending on instructional costs, including on teacher salaries.

- Forty percent of public school teachers do not participate in Social Security, but they should be. Back in the 1990s, Congress attempted to ensure that non-participating workers had benefits that were at least as generous as Social Security, but the implementation of that rule has been botched by the IRS, leaving too many workers unprotected from years of low retirement saving.

I could go on. But rather than holding up teacher pensions as a space worthy of emulation, Congress should be holding hearings on some of these issues.