Last week was Veteran’s Day, and as we honor the security provided by those who served our country, we should also consider the retirement security of those who serve. While government initiatives through the GI Bill provide veterans with generous benefits such as education reimbursements, on-the-job training, and low-interest mortgages to help them successfully transition back to the civilian world, retirement benefits remain surprisingly inadequate for many of those who serve.

Alongside teachers and other state workers, the military is one of the few remaining occupations that still relies on a traditional pension. Like the plans offered to teachers, military pensions do not distribute benefits equally—severely shortchanging the majority of members—and their costs are high and unpredictable. The Department of Defense is now considering switching to a hybrid model that would combine a less-generous pension with a more portable 401k-style plan.

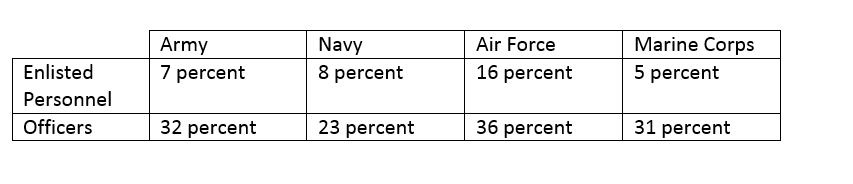

Currently, members of the Armed Forces participate in Social Security and a defined benefit pension plan. Similar to state pension plans for teachers and other government workers, benefits are calculated based on a formula that multiplies a member’s years of service by final average salary and a multiplier, 2.5 percent for military veterans. In order to qualify for this benefit, an Armed Forces member must serve a minimum of 20 years. According to a recent RAND report, 66 percent of officers and 86 percent of enlisted personnel will not stay long enough to receive these retirement benefits. The numbers are even steeper when separated by individual service branches:

Percentage Who Qualify for Military Pension Benefits Under the Current 20-Year Vesting Requirement

Within the Army, the largest branch of the Armed Forces, 93 percent of enlisted personnel and 68 percent of officers will not receive a pension. This is so shocking that it bears repeating: The majority of those who serve our country will leave with zero pension retirement savings.

According to RAND, the Department of Defense can significantly improve retirement security while saving between $1.8 billion and $4.4 billion dollars annually by adopting a hybrid retirement model. Rather than relying so heavily on a back-loaded pension, the recommended hybrid model has four streams of income: a smaller defined benefit pension, Social Security, a defined contribution or 401k-like plan called the Thrift Savings Plan (TSP) that’s currently offered to civilian federal employees, and upfront bonuses for longevity paid out in cash. By decreasing the size of the pension benefit, members would receive an additional source of retirement income from the TSP and more upfront compensation through cash bonuses for certain longevity milestones (e.g., 12 years of service) or increased transition pay for those who serve for 20 years. The 20-year vesting period would remain the same for the traditional, smaller pension component. However, the TSP would have a lower vesting period of 6 years and would include an automatic 5 percent employer contribution, allowing more military members to leave with adequate retirement benefits.

According to the Department of Defense’s actuaries, the new model would not diminish the military’s capacity. Slightly more members would remain in the earlier years and slightly fewer members would stay after 20 years. Essentially, though, a hybrid plan would offer better benefits without altering who would serve.

The military remains one of the few federal agencies not already offering a more portable retirement benefit. Almost all federal workers today participate in a hybrid retirement plan, which itself replaced an outdated pension system and has provided employees with secure, portable retirement benefits. It may be time for the Armed Forces to follow suit.