State pension plans are shouldering a collective shortfall of $1.3 trillion dollars in unfunded liabilities. While the recent recession took a large toll on plans, however, other factors like inadequate contributions are also to blame.

The Center for Retirement Research (CRR) recently released a report quantifying the factors that led to state and local plan underfunding. The CRR tracked five specific factors in 150 public plans from 2001 to 2013: 1) investment returns; 2) plan contributions; 3) actuarial assumptions; 4) benefit changes; and 5) other assumption changes. Using this data, CRR looked at how each of these factors impacted a plan’s unfunded liability over time.

Low investment returns and inadequate contributions were the top two factors impacting a plan’s unfunded liability. Plans faced two financial crises over the past two decades, once in the early 2000s when the dot-com bubble burst and again after the financial downturn in 2007-9. But this doesn’t tell the whole story. While the recession hurt all plans, poorly funded plans that were skimping or skipping contributions fell much further than well-funded plans. Overly rosy investment assumptions also didn’t help.

A good example is the New Jersey Teachers Retirement System (TRS). New Jersey hasn’t made adequate contributions to cover the annual cost of benefits, let alone the plan’s unfunded liability, since the 1990s.

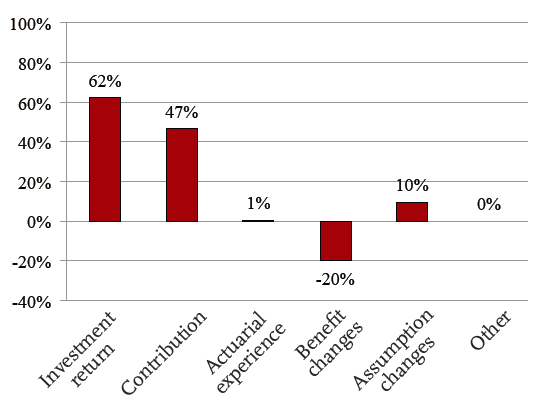

Low investment returns impacted New Jersey’s unfunded liability by over 60 percent. But poor management in the form of missed and cut contributions played a key role in New Jersey’s current status, changing the state’s underfunding by almost half. Overly optimistic demographic and investment assumptions also increased the unfunded liability. The chart below shows how much these and other factors like increasing or decreasing benefits or changing assumptions (i.e., interest smoothing or gradually adjusting interest rates incrementally)—impacted the New Jersey Teachers’ Retirement unfunded liability.

Factors Impacting the New Jersey Teachers’ Retirement System’s Unfunded Liability, 2001-2013

Source: Alicia H. Munnell, Jean-Pierre Aubry, and Mark Caferlli, “How Did State/Local Plans Become Underfunded?”, Center for Retirement Research, 2015. The graphs show the percentage of overall change in the aggregate Unfunded Actuarial Accrued Liability (UAAL).

For most plans, the main factor driving unfunded liabilities were low investment returns that fell short of what plans were expecting. But another serious factor was failing to make adequate contributions, especially for the worst-funded plans (like New Jersey). While missed contributions accounted for close to half of New Jersey’s poor funding, for a better-funded plan like Georgia, missed contributions only impacted the plan’s unfunded liability by 18 percent.

It’s clear that states need to change how they are managing their public retirement plans. While stock market returns are unpredictable, states should be more responsible on the things they do control, like good funding practices.

Taxonomy: