Last In, First Out (LIFO) policies prioritize seniority when a district must make reductions to its teacher workforce. The last teachers hired are the first ones with pink slips.

Unfortunately, this practice of favoring seniority at the cost of early career teachers extends to pensions, albeit in a slightly different form. More often than not, benefit cuts fall on new teachers.

Many states protect public sector pension benefits with strong, near ironclad legal rules that make it tough-to-impossible to reduce benefits for existing workers. Many state constitutions and statutes explicitly protect the existing, and sometimes even future unearned benefits, of teachers. These protections are good for teachers already in the system, but when tough budget times hit they often leave states with no other choice but to cut benefits for those just joining.

States may trim other benefits for current workers, reducing cost-of-living adjustments, or COLAs, which adjust benefits for inflation. But even still, states continue to struggle with gargantuan underfunding and look for other avenues for cuts. A few headstrong legislatures, such as Illinois and New Jersey, are trying to reduce or freeze benefits for existing workers despite strong legal protections. Illinois is now in the throes of a legal battle over its changes. It’s unclear whether New Jersey’s proposal will move forward. Rhode Island may be an exception.

So in order to avoid the political and legal headache of trying to cut benefits for existing workers, states typically take the easier path and create new “tiers” or modified versions of a plan with lower benefits for new teachers. All new teachers hired after a specific date are put into the different tier with reduced benefits, while senior teachers hired before the date remain in the better, more generous plans they were hired into. Over 40 states place teachers in separate tiers by their hire date according to the Urban Institute’s state report card.

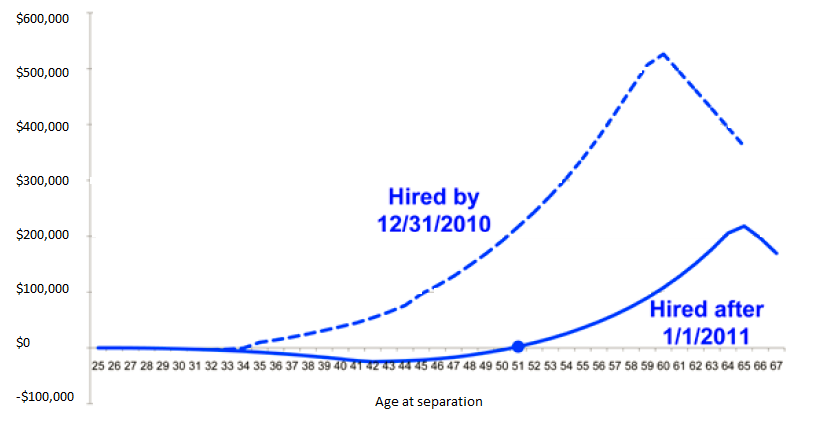

Illinois provides an illustrative example. In 2011, Illinois passed legislation creating a “tier 2” plan for new teachers. Tier 2 offers worse benefits for new teachers: it has a higher minimum service requirement (up from five to 10 years, making it more difficult for new teachers to qualify for a minimum benefit), a higher normal retirement age (meaning teachers have fewer years to collect pension payments over a lifetime), a less generous pension formula (calculating the final average salary from the last eight years of service instead of just four), and a lower COLA. The graph below comes from a report by Robert Costrell and Mike Podgursky, and looks at the net pension benefits for Illinois teachers before and after cuts. The top, dotted, curve shows benefits for existing teachers hired before 2011. The lower, solid curve applies to new teachers hired after 2011.

The gap between the plans is large. Existing teachers are protected, while new teachers bear the brunt of the reform cuts. For new teachers, pension wealth is actually negative for the first 25 years a new teacher teaches under tier 2. Despite lower plan benefits, new teachers still need to contribute the same percent of employee contributions as more senior teachers, reducing overall net pension benefits even more.

Net Pension Wealth for Illinois Teachers

Source: Robert Costrell and Michael Podgursky, “Reforming K-12 Educator Pensions: A Labor Market Perspective,” TIAA-CREF Institute, February 2011. Shows pension wealth accrual, net of employee contributions, adjusted for inflation, for a 25-year old entrant.

Compounding the LIFO effects between tiers, the traditional pension structure inherently favors late- over early-career teachers. Unlike other retirement savings plans, traditional pensions aren’t directly tied to a teacher’s contributions. Instead, pension formulas largely hinge on two main factors: a teacher’s time in the classroom and their average salary just before retirement. As a result, the bulk of a teacher’s retirement wealth is earned at the back end of her career, if she makes it that far.

There’s a significant chasm between what early- and late-career teachers earn in retirement benefits. In New York City, a public school teacher who begins at age 25 earns roughly $3,500 per year for the first 20 years she teaches. If she works for an additional 18 years, she earns $30,000 per year during these later years. In Illinois, a teacher who begins at age 25 and works for 10 years accumulates $28,000 in overall lifetime benefits; a teacher with 35 years peaks at $1.3 million. Needless to say, pensions aren’t evenly distributed.

But to be clear, while policy recommendations for revising Last In, First Out layoff decisions generally means tying a teacher’s job to her performance, adequate retirement benefits should be offered to all teachers as part of an attractive compensation package. All teachers deserve secure retirement benefits, period.

States need to pause and consider how cuts unevenly impact teachers. Simply cutting benefits for new hires can’t continue forever.

In the upcoming months, TeacherPensions.org will be releasing a report that looks at changes that state pension plans have made over the past few decades. Check back here for our analysis of those cuts and the impact on the teaching profession.

Taxonomy: