Call it the chart that launched a conference. In 2007 Robert Costrell and Michael Podgursky released a report called “Golden Peaks and Perilous Cliffs: Rethinking Ohio’s Teacher Pension System.” The report, and the attention spawned by it (including a dedicated research conference), was driven by one chart.

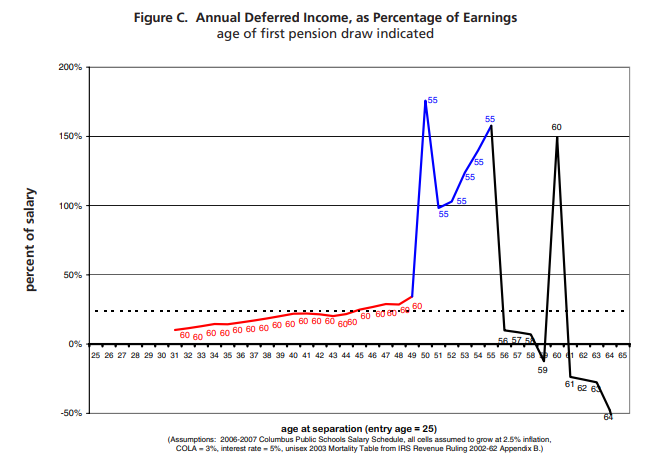

The chart shows the retirement wealth accrual over time for teachers. The report’s title is evocative of the chart; namely, it demonstrates vividly the enormous financial pressure teachers face at various stages of their careers. Podgursky, Costrell, and others have since drawn similar charts for a number of states, and they all show how teacher retirement accounts grow slowly over time, only to spike dramatically at various ages determined by state pension plan formulas. Ohio’s, the first of the state charts and the one below, has two such spikes, one for an early retirement incentive and again at the “normal retirement age.” In the chart below, the hypothetical teacher who enters teaching at age 25 gains over $100,000 in future pension wealth at age 50, 55, and 60. Every year they choose to work past age 60, they forfeit pension wealth, meaning they’re actually losing money by working additional years.

Not surprisingly, these peaks correspond neatly to retirements: teachers do respond to the incentives, and they are, for the most part, retiring when the retirement formulas tell them to do so. Research from California shows that teachers changed their retirement age to 61.5 (an unusual retirement age) in response to changes in the state’s retirement structure in the late 1990s. In an era when Americans in general have been retiring at later ages (due to declines in average pension and Social Security wealth), teachers have been retiringyounger.

So there I was spending two days in Nashville discussing these peaks and how, if, or whether they could/should be fixed. With the Dow and the S&P 500 plunging to six-year lows, it was an interesting time to be having the discussion.

With only a few exceptions, most teachers have defined benefit (DB) pension plans. This means they are guaranteed retirement benefits determined by a formula, which are almost always derived by multiplying some replacement factor (typically 1-3%) times years of service times average final salary. If a teacher lived in a state with a constant replacement rate of 2% and retired after 25 years on the job with a final average salary of $50,000, her benefits would look like this:

Monthly benefit = (.02 X 25 X 50,000)/ 12

Monthly benefit = $2,083.33

DB plans were once common in the private sector too, but their frequency has fallen since the mid 1970s. They have been replaced by defined contribution (DC) plans. DC plans, like their name, define the retirement contribution an employer makes on an employee’s behalf. In most DC plans, the employer contributes a certain percentage of an employee’s wages into a 401(k) account.

The conference at times devolved into a DB versus DC debate, but before I get into why that’s a false choice, I’ll take some time to weigh their strengths and weaknesses.

DB plans allow individuals to make predictable estimates of their retirement wealth. Since they are usually accompanied by cost-of-living adjustments, they should not erode significantly because of inflation. They last until the individual passes away. They pool risk, so that the fund can make wise, long-term investments. And when a recession hits, current teachers and all taxpayers bear the responsibilities of DB benefit promises. If their goal is to provide a secure retirement as a reward for a career of service, they do their jobs.

At the same time, DB plans transfer wealth from mobile workers to non-mobile ones (mobile workers contribute but never capture the full benefits that longevity assures), from young to old (the young pay into a system that backloads rewards), and from men to women (women live longer and thus earn benefits for more years). (As an aside on teacher quality, DB plans promise nothing to prospective teachers who want to try out the profession. If they leave before being “vested,” usually after five or ten years, they get nothing.) State-run DB plans are subject to interest group influence, which has caused rising payout rates and given teachers more generous pensions over time, especially when compared to private-sector workers. Worst of all, public sector DB plans are typically locked in. A state that increases pension benefits during boom times cannot rescind this offer during boom cycles. In fact, in many states, pension benefits can never be reduced from the time a teacher begins their career.

DC plans offer an alternative. They give every employee the same percentage of salary contribution. In this way, they make it much easier for employers to project future obligations. Individuals have choices; they can participate if they want to or not, invest as they please, and take the money with them when they leave. There is no “maximum” DC pension wealth, because the contribution stays the same regardless of age or service. If a teacher passes away prematurely, her heirs inherit what remains of the account.

Or, the money in a DC plan could run out. Individuals tend to do a bad job of investing, not saving enough, not diversifying their portfolio, investing in too risky or too conservative assets. DC plans are also subject to the whims of the business cycle, since an employee must reduce risk as they near retirement. All of these factors make DC plans less efficient; DB plans often earn investment returns one to two percentage points higher than DC participants.

Ultimately, the DB plans suffer from two main things. One is the aforementioned peaks, and the other is portability. Both are fixable.

The peaks of the current systems are a serious problem. They pull bad teachers to stay in the profession too long, just so they’re able to earn a full pension. And they push out teachers who want to stay in the profession, because of the severe financial penalties on teachers who opt to stay in after their “normal retirement age.” But peaks are not unique to DB plans. Employees with DC plans time their retirement decisions to coincide with high market values of their accounts. Alternatively, we’re now seeing stories of people delaying retirement because of current economic conditions. Of the two, DB plans are the ones that are not inherently linked to peaks.

Politicians like to reward active interest groups with tangible benefits, especially if those benefits are obligations only at some time in the future. Teacher pensions fit this precisely: their unions have significant influence on state politics, and a promise for pension benefits accrues to members slowly over time. Current politicians saddle future ones with the budget problems while satisfying an interest group. In an analysis of the actions of Missouri’s state legislature, which increased teacher pensions nine times during a ten-year period from 1991-2001 (netting each teacher about $75,000 in future benefits and imposing a $5.4 billion long-term liability to the state), researchers saw little evidence of any real analysis. The economy was running smoothly, so state legislators spent as if there were not going to be tech or housing bubbles looming in the next decade.

Other states have taken similar paths, making reform seem impossible, but two states have experimented with legislation that has introduced sanity to the process. Oklahoma and Georgia now have laws on the books requiring a two-year deliberation period before making any changes to the state pension plan. The state must create an analysis at the front-end of the impacts of the proposal, update the analysis after an additional year, and then pass the legislation. Legislators are no longer able to commit the state to large future budgetary obligations without two full years of deliberation.

The second problem with DB plans is interstate portability. Because benefits accrue slowly over time, a teacher who splits her years of service between two states will earn a significantly smaller pension than someone with the same number of years of service in only one state. Researchers at the conference found a hypothetical teacher with 15 years of service in each of two states would accumulate 35-65% less pension wealth than one who stayed put. Thus far, mechanisms to increase portability mostly fail. Teachers can cash out of the first pension program to purchase additional years of service, but in the process they often must forfeit all of the employer’s contributions in the process. These are substantial sums, since employers often contribute the majority of the fund. Some states even mandate the teacher forfeit any earned interest.

But these rules are not fixed in stone. In reality, these prohibitive rules are in place for nothing other than to enrich the state fund on the backs of teacher-leavers. States have no real incentive to fix them now, but they could form partnerships across borders to agree to more equitable rules for interstate movers. If this didn’t work, the federal government could threaten a pension fund’s tax-exempt status if it refused. Or, employers could begin offering a form of DB plan called cash balance (CB). CB plans guarantee individuals a (generally low) return on their investments and typically require the employer to contribute some percentage of the employee’s salary. The account is in the employee’s name, but the benefit–the interest rate and contributions–are guaranteed, placing the risk with the employer. An employee can choose whether to take the account balance as a lump sum payment or transfer it to a lifetime annuity.

Ultimately, the peaks and portability problems are the largest barriers to the status quo. Because while defined benefit retirement plans for government workers often come under scrutiny for being too generous(including and especially those of teachers), it’s important to think about the goal of any retirement system. Defined contribution plans might be better if the goal is to minimize cost and risk to the employer while giving the employee maximum flexibility. But if it is to create a loyal workforce with the prospect of a secure retirement, then defined benefit plans are quite successful.

This blog entry first appeared on The Quick and the Ed.

Taxonomy: