The New York Times recently covered a story about a 57-year-old woman, Gail Ruscetta, who switched careers to become a teacher in Virginia. Retirement security is important for all workers but is particularly salient for individuals nearing retirement age and moving into a second career in their late fifties. Unfortunately for teachers like Ms. Ruscetta, most state pension plans are designed primarily to support the retirement of teachers with a much longer time to serve. Her retirement benefits will be relatively modest in comparison.

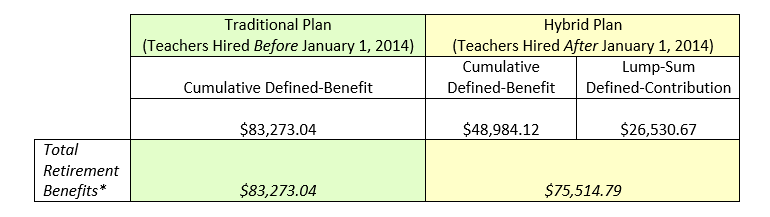

As a teacher beginning in 2012, Ms. Ruscetta is covered under a traditional defined-benefit plan. The traditional pensions benefit is calculated by multiplying a teacher’s final average salary by a 1.7 multiplier by years of service. After five years of service, Ms. Ruscetta will qualify for a yearly pension benefit of roughly $4,600, or about $83,000 for her entire retirement. Benefits earned at this stage of a career are unlikely to be sustainable by themselves.

Ms. Ruscetta coincidentally entered the teaching workforce right at the cusp of reform. In 2012, Virginia passed an overhaul of the state retirement system. Under the new law, teachers hired on or after January 1, 2014 must enroll in the state’s hybrid plan. The state’s new retirement plan consists of a less-generous defined-benefit component than the one found in the old pension system, as well as a defined-contribution component similar to the 401(k) plans found in the private sector. Teachers hired before January 1, 2014 retain the traditional defined-benefit pension plan or can choose to opt into the new plan. Had Ms. Ruscetta began working in the 2014-15 school year, she would have been automatically covered under the new plan.

As a hypothetical, let’s look at how retirement earnings under the traditional plan compare to the new hybrid plan. The hybrid plan has two streams of retirement benefits. Assuming she contributes the maximum 5 percent (which the state matches at 3.5 percent) and a 6 percent investment rate, the hypothetical teacher would accumulate around $26,500 after five years in the defined-contribution portion of the plan. She could receive the $26,500 as a one-time lump sum, spending the amount however she chooses. In the defined benefit portion of the plan, she would receive a yearly benefit of $2,700. This $2,700 is an annuity, meaning that she would receive $2,700 on a yearly basis beginning at age 65 and each subsequent year of her life for a cumulative benefit of about $49,000 (unadjusted for inflation).

Retirement Benefits (With 5 Years of Service)

The traditional defined-benefit plan would provide Ms. Ruscetta with a higher annuity and total retirement benefits than the new hybrid plan, but only if she stays at least five years. If Ms. Ruscetta (or any teacher) leaves before five years, she would relinquish rights to a pension altogether, and leave with just her original contribution and accrued interest. The hybrid plan, in contrast, allows new teachers to retain 50 percent of the employer contribution after two years, 75 percent if they leave or move after three years, and 100 percent after four years.

The state retirement system estimates that half of all teachers who begin teaching at age 25 will leave the system after five years and 73 percent will leave before 10 years. The state estimates higher retention rates for teachers entering the classroom at older ages, but they still have relatively high turnover. For teachers who enter Virginia public schools at age 55, the state estimates that 64 percent will remain in the classroom after five years and 50 percent will remain after 10 years. Given these retention statistics, the new hybrid plan provides transient and short-term teachers greater retirement benefits (as opposed to just their own contributions). Whether the hybrid plan itself could create an incentive for increased turnover is up for debate and an area for research.

What does this all mean for Ms. Ruscetta? We certainly hope the odds are in her favor to stay in the classroom as long as she likes, but it’s understandable that a 55-year-old may want to retire at a reasonable and comfortable age. While Ms. Ruscetta’s pension benefits greatly increase with additional service years (her annuity would rise to $11,000 after 10 years or $30,000 after 20 years), her chances of remaining in the classroom become slimmer and slimmer with each passing year. Plus, at some point she has a diminishing return because each year she continues working is a year she can’t enjoy retirement. Only a small percentage of teachers like her stay in the classroom for long enough to qualify for the greatest benefits of the pension system and become “pension millionaires.”

*Benefit calculations are based on the Alexandria Public Schools’ salary schedule for teachers serving 205-day calendar years. Does not include cost-of-living adjustments. Virginia grants cost-of-living adjustments (COLA), matching the first 2 percent increase in the Consumer Price Index for all Urban Consumers and half of any additional increase up to 2 percent, for a maximum COLA of 3 percent.