The following is a guest post from Ryan Frailich, a Certified Financial Planner. He started his career teaching in Mississippi, before moving to teach in New York City and then New Orleans. In the first decade of his working career, Ryan ended up with one state pension and three different 403(b) plans. Upon researching his situation and learning more about the state of retirement for teachers, Ryan switched careers and then became a financial planner with a focus on helping young couples and educators plan for their financial lives.

The chart below is something everyone “knows,” but most people forget about for 99 percent of their lives. Inflation, a concept all of us are exposed to in high school economics class, is the slow moving force behind those stories your grandfather told you about going to the movies for 25 cents, or buying a bottle of coke for a dime. Yet when it comes to the impact on teacher’s retirement plans, people are in the dark.

Teacher pensions are a struggle to write about because there’s a chasm between what’s promised and the outcomes for the overwhelming majority of teachers. I believe all teachers should get the benefits promised to them, but here in the real world, we have to face the fact that the commonly held notion of a teacher working 30-35 years and retiring with a gold plated pension is largely fiction. The small number of teachers who actually reach breakeven has been widely covered, not to mention the even tinier fraction of beginning teachers who actually reach full retirement age. Setting aside those issues for a moment, let’s take a look at what happens to a teacher who starts in a retirement system, spends 30 years in it, and retires.

I’m in Louisiana, so let’s take a teacher who started in 2018 in the Baton Rouge schools. Let’s call this teacher James. James is 22, right out of college, and the starting salary for a brand new classroom teacher is $44,500. James stays in the district his entire career, earns a Master’s degree along the way, and retires 30 years later with a peak salary of $67,200.

Using the Teacher’s Retirement System of Louisiana’s pension calculation, we calculate his benefit the year after he retires as follows:

Years Worked * Pension Multiplier * Highest three years average salary

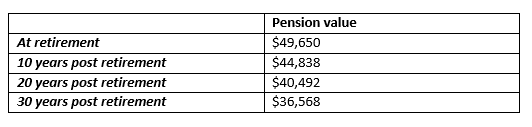

30 * 2.5 * $66,200 = $49,650

Wow! He can stop working and go on collecting $49,650 from age 53 until whenever he passes away. Or can he?

Enter the inflation monster.

History isn’t entirely predictive, but let’s use historical inflation to see what happens to the real dollar value of James’ pension over time. The consumer price index rose 2.54 percent per year, on average, from 1988-2018, so we’ll use that as our estimate of the next 30 years.

Technically, TRSL offers a cost of living adjustment that can be about 1.5 percent per year, so we’ll factor that in for now. As we’ll get to later, that’s another one of those things that’s promised on paper until you read the fine print.

With the numbers cited above, the table below captures the current value of his pension at ten year increments into the future.

Ugh. Now, at 82 years old, James has to find a way to make up for the fact that his pension has lost 26.3 percent of his purchasing power to inflation since he retired.

The above assumes that TRSL awards that 1.5 percent cost of living increase every year, but historically that hasn’t been the case. TRSL has rules governing when a cost of living increase can be awarded, and those rules are incredibly complex, but essentially hinge on 3 things:

The funded ratio of the plan

The past year’s investment returns &

approval from the state legislature.

Translation: It’s not happening annually. In 2016, Louisiana teacher retirees got their first cost of living adjustment in eight years, and it was 1.5 percent. If we know his pension loses 26 percent of its value while getting a yearly cost of living adjustment, imagine how bad it looks if he only gets one every eight or so years.

This scenario I’m presenting is, in all reality, the best case scenario for many teachers in Louisiana. There are a variety of other scenarios in which the payout looks even worse.

It’s worse because whatever meager Social Security a teacher in Louisiana may be eligible for would get reduced due to the windfall elimination provision. I say meager because years spent teaching in Louisiana are years not spent contributing to Social Security, so career teachers may only have sporadic income from college or post retirement to earn Social Security credits.

It’s worse because just over one quarter of teachers who enter the system even get to the roughly 20 years required to break even, adjusted for inflation, on their own contributions. And if you leave the system, the amount you can withdraw and put in your own IRA has sat, uninvested, without interest, for years.

It’s worse because if you decide to leave your contributions with the state of Louisiana, and draw your pension in the distant future, inflation erodes it all along the way. Say James stops teaching after 15 years and changes careers, but wants to draw his pension. The pension won’t be accessible for him until age 62 (age 60 for some retirees). Those 24 years of inflation at 3 percent leave what would’ve been an annual payment of $19,331 worth just $9,306 per year.

It’s worse because the Louisiana pension has been underfunded for years, so at some future, indeterminate point, it’s possible the benefits that do exist will be reduced.

If one of the best outcomes for a new teacher entering the system is one in which their pension payout loses 26 percent of its value over a 30 year retirement, then thousands of teachers get even worse.

What You Can Do About It

There are a host of policy changes I’d love to see, but for this article, let’s stick to what’s in your control.

- Max out a ROTH IRA. I encourage all teachers to contribute to a ROTH IRA, and work to max out the annual limit whenever possible. This will give you a post-tax pot of money to draw on and supplement your pension in retirement years.

- Use the 457 or 403(b) Plan (with caution). Most districts have either a 403(b) plan, a 457 plan, or both. These are retirement plans that allow you to put much more money in each year than an IRA. But use caution because 403(b)’s are rife with horrendous investment options and investment fees I wouldn’t wish upon my worst enemy. Do your homework before committing to one of these plans, but when you find a good one with reasonable fees and adequate investment options, it will provide a tool to start building money you can rely on if your pension falls short of fully meeting your long term needs.

- Adjust your expectations. New teachers need to go in with eyes wide open, and know that the odds are against them in getting the gold plated pension. Being clear eyed about this helps people know well in advance, and better prepare for it.

- Decide on a career path early. This is hard because my advice is to decide in the first few years of your career whether you’re going to stick with it for the long haul or not. That is obviously easy to say but much harder to implement given all the life variables that come peoples way. That said, if you are going to make a full 20+ year career of teaching in one state, you’ll do okay with your pension. If you work 2-4 years and move on, the decision to withdraw your contributions and invest in an IRA is easy. The challenge is hardest for people who have 8-15 years in the system, and either way they choose comes with significant downsides.

To me, it’s a shame that so many teachers will end up having inadequate resources to retire on. If I could wave my magic wand and give teachers a pension option that met the needs of the majority of teachers, I would do it in the blink of an eye. Teachers deserve better than the disjointed, underfunded, and inadequate system most have access to.