Pennsylvania announced earlier this month that the contribution rate for its teacher pension plan will rise from 30.03 percent of salary last year, to 32.57 percent next year. Although that 33 percent employer contribution rate is already insanely high, it's scheduled to continue rising in the years that follow. By the 2021-22 school year, Pennsylvania school districts will pay 36.4 percent of each teacher's salary into the pension fund.

To be clear, most teachers will never see this money. Most Pennsylvania teachers don't stay long enough to qualify for benefits worth even as much as their own contributions, let alone the state's sizable contributions. The vast majority of the contributions are for debt that the state has accured after years of over-promising and under-saving. Billions of dollars a year must come out of state and district education budgets in order to pay down these debts.

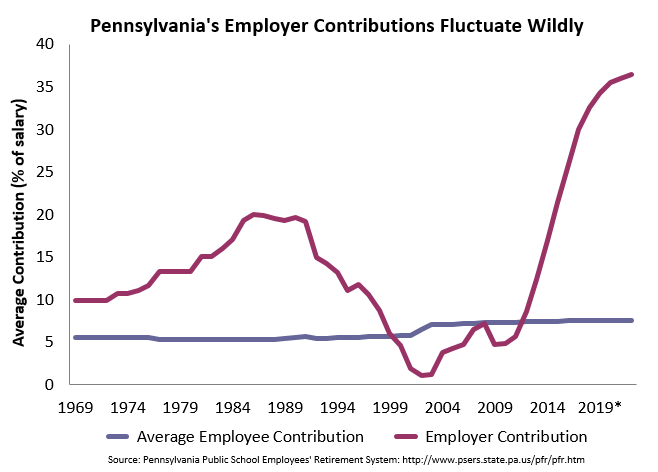

Graphically, Pennsylvania's employer contribution rates look like a roller coaster (see graph below). A scary, painful roller coaster. While teacher contribution rates have increased only a bit, state and district contribution rates are much more volatile. They rose throughout the 1970s and 80s, then the unprecedented stock market boom in the 1990s allowed state pension contribution rates to fall all the way to 1 percent in 2002. Around that same time, pension plan assets looked flush, and so the state enacted a large retroactive benefit increase for teachers and retirees.

Those turned out to be terrible mistakes based on flawed assumptions. First the dot-com bubble burst, and then the Great Recession hit, and now Pennsylavania's teachers, schools, and taxpayers are paying the price.

Where will this roller coaster go next? Advocates of the current system suggest a wait-and-see approach. They argue that the state can't afford to get off, because the pension plan needs new money from new teachers.

It's true that Pennsylvania can't just pretend it never created this roller coaster. The unfunded pension liabilities are real and aren't going away. In fact, they'll remain even if the state hits its assumed investment target of 7.5 percent, and they'll grow if the state fails to hit that target. Meanwhile, it's not good for Pennsylvania's current or future teachers to ask them to pay down the pension debts through what is, essentially, a tax on their labor.

Instead, Pennsylvania should recognize that its pension debts were created by past state legislatures and governors, and the entire state should carry the burden of paying those off. That could involve other, dedicated sources of revenue, but it's unfair to keep forcing new teachers into an expensive, volatile, fundamentally flawed retirement plan. Pennsylvania can't afford to keep riding this particular roller coaster, and it nees to find a responsible way to shut it down.