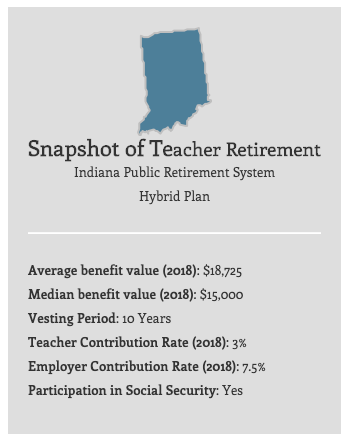

Snapshot of Teacher Retirement

Indiana Public Retirement System

Hybrid Plan

Average benefit value (2018): $18,725

Median benefit value (2018): $15,000

Vesting Period: 10 Years

Teacher Contribution Rate (2018): 3%

Employer Contribution Rate (2018): 7.5%

Participation in Social Security: Yes

How Does Teacher Retirement Work in Indiana?

In Indiana, teachers are a part of the Indiana Public Retirement System, which includes not only teachers but all state employees.

But unlike most states, new teachers in Indiana have a choice about their retirement plan. New teachers are by default enrolled in the Teachers' Retirement Fund Hybrid Plan, which combines elements of a traditional pension plan and a defined contribution (DC) plan. Or, new teachers can elect to join Indiana's My Choice: Retirement Savings Plan. For new hires, their retirement plan selection must be made within 60 days of their start date.

Although it only comprises part of the hybrid plan, the basic structure of Indiana's defined benefit (DB) pension is similar to that of other states. Unlike other retirement funds, a teacher’s contributions and those made on their behalf by the state or school district do not determine the value of the pension at retirement. Although those contributions are invested in the market, the pension wealth component of the overall hybrid plan is not derived from the returns on those investments. Instead, it is determined by a formula based on their years of experience and final salary.

How Does Indiana's My Choice: Retirement Savings Plan Work?

This is a traditional defined contribution (DC) plan, in which the employee and the employer contribute annually a share of a teacher's salary to the fund and the worker's retirement wealth is determined by those contributions and the interest they earn. Each year a teacher contributes at minimum 3 percent, and no more than 10 percent, of their salary to the fund. Their employer contributes 5.3 percent annually. Teachers only vest into the system gradually, meaning that they're eligible for a share of the employer contributions based on their years of experience. After their first year, a teacher is eligible for 20 percent of the employer contributions. Each year thereafter, they can access an additional 20 percent. After 5 years, a teacher is fully vested.

This leads to another important element of Indiana's My Choice plan: it is fully portable. This means that teachers who leave Indiana to teach in another state can bring all their vested retirement funds with them. Teachers enrolled in a pension plan cannot do this, which likely results in much lower retirement earnings over their career if they move across state lines.

How Does Indiana's Hybrid Plan Work?

Teachers who elect to join Indiana's Hybrid plan, or who are enrolled into the system by default, contribute at least 3 percent and no more than 10 percent of their salary annually to the fund, while their employer contributes 5.5 percent of salary to the defined benefit portion of the system. As a result, between 8.5 and 15.5 percent of a teacher's salary is contributed to their retirement account annually. However, when a teacher retires the total value of the DB portion of the plan is determined by formula based on years of experience and a teacher's final average salary. Greater detail on the pension formula is provided in the section below.

Under the Hybrid plan, teachers vest for the DB portion after 10 years of service. But unlike the My Choice plan, should a teacher leave the classroom, even if they are fully vested, they will only be able to bring the contributions they made themselves across state lines. In other words, this plan is only partially portable.

How Are Teacher Pensions Calculated in Indiana?

Pension wealth is derived from a formula. The figure below illustrates how a teacher pension is calculated in Indiana. It is important to note, however, that the state assesses an educator’s final salary based on their highest 5 years average salary. For example, a teacher who works for 25 years with a final average salary of $70,000 would be eligible for an annual pension benefit worth 27.5 percent of their final salary. But keep in mind the DB plan is only a portion of a teacher's retirement benefit under the hybrid plan.

Calculating Teacher Pension Wealth in Indiana

| 1.1% Multiplier | X | Avg. highest 5 years of salary | X | Years of service |

Who Qualifies for the Pension Portion of Indiana's Hybrid Plan?

Like most states, teachers need to serve a number of years before qualifying for a pension. For new hires participating in the hybrid fund, Indiana has a 10 year vesting period. While educators qualify for the pension portion after 10 years of service, the pension may not be worth all that much. Moreover, educators can’t begin to collect it until they hit the state’s retirement age.

The state sets specific windows when teachers can retire with benefits based on age and years of experience. New teachers starting out in Indiana can retire with their full benefits at:

- Age 55 with 30 years of service;

- Age 60 with 15 years of service; and,

- At age 65 with 10 years of service.

Additionally, Indiana allows early retirement from age 50 to 59 once a teacher has 15 years of experience. However, teachers taking that option will have their benefits reduced.

How Much Does Indiana's Pension System Cost?

As they work, teachers and their employers must contribute into the plan. Those contribution rates are set by the state legislature and can change year-to-year. In 2018, teachers contributed at least 3 percent of their salary to the pension fund, while the state contributed 7.5 percent. At minimum, 10.5 percent of teacher salary was spent on Indiana's teacher pension fund. However, not all of that investment goes toward benefits. While the full amount of a teacher's own contribution is for benefits, the state contributes only 5 percent toward benefits. The remaining 2.5 percent state contribution is to pay down the pension plan's unfunded liabilities.

As with most state pension funds, Indiana's hybrid teacher retirement system provides the greatest benefits to teachers who stay the longest, while leaving everyone else with inadequate benefits. With that in mind, teachers participating in Indiana's hybrid plan should think carefully about their career plans and how they interact with the state's retirement plan.

Glossary of Financial Terms

Vesting period: The number of years a teacher must teach before becoming eligible to receive a pension. Although the length of vesting periods vary by state, 5 years is typical. In every state, a teacher who leaves prior to vesting is eligible to withdraw his or her own contributions, sometimes with interest, but few states allow those employees to collect any portion of the employer contributions made on their behalf.

Employee contribution: The percent of a teacher’s salary that he or she pays annually to the pension fund.

Employer contribution: The percent of a teacher’s salary that the state, school district, or a combination of the two pays annually to the pension fund.

Normal cost: The annual cost of retirement benefits as a percentage of teacher salary. This excludes any debt cost.

Amortization cost: The annual cost of a pension fund’s contribution toward any unfunded liabilities. This can also be thought of as the debt cost of the pension fund.

https://www.teacherpensions.org/state/indiana